What Your $100 Card Payment Actually Pays For

You tap. Money moves. But not all of it.

You walk into a coffee shop in Singapore. You order a flat white. The barista says "$5.50." You tap your Visa card on the terminal. The screen flashes "Approved." You take your coffee and leave.

Behind that tap, something happened that most people never think about. Your bank didn't just move $5.50 from your account to the coffee shop's account. Before the money arrived, several parties each took a small cut. The largest of those cuts has a name: the interchange fee.

For a $5.50 transaction, the coffee shop might receive about $5.36. That missing $0.14 pays for the infrastructure that made the tap work: the fraud detection, the card network, the processing, and the rewards program that gives you cashback on your morning coffee.

Multiply that $0.14 across billions of card transactions worldwide, and you're looking at over $160 billion a year in the US alone. Globally, interchange is a multi-hundred-billion-dollar transfer from merchants (and ultimately, from you, through slightly higher prices) to the banks that issue your cards.

Yet most people, including many who work in payments, cannot explain what the fee actually pays for.

This is that explanation.

The four parties at the table

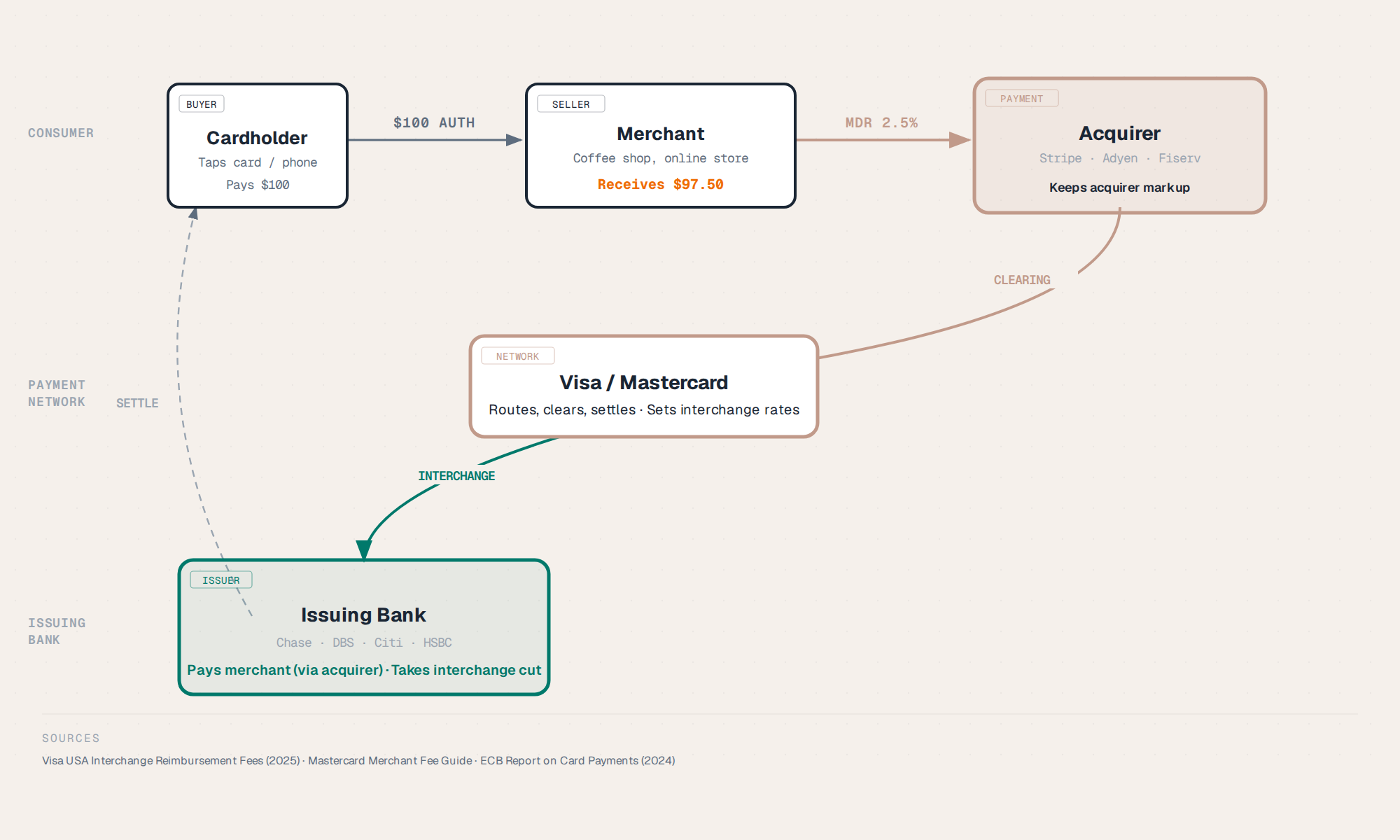

Every Visa and Mastercard transaction involves four parties. Not three. Not two. Four. Understanding who they are is the foundation for understanding interchange.

First: you, the cardholder. You carry the card and initiate the payment.

Second: the merchant. The shop, restaurant, or online store where you're buying something.

Third: the acquirer. This is the merchant's bank, or more precisely, the financial institution that processes card transactions on the merchant's behalf. Companies like Stripe, Adyen, and Square are acquirers (or work with acquirers). When the terminal says "Approved," the acquirer is the one who received that message from the card network and passed it to the merchant.

Fourth: the issuer. This is your bank, the one that gave you the card. DBS, Chase, Citi, UOB. The issuer extends you credit (if it's a credit card), takes the fraud risk if someone steals your card, funds your rewards program, and guarantees payment to the merchant even if you never pay your bill.

Connecting all four parties are the card networks: Visa and Mastercard. They don't issue cards and they don't bank merchants. They operate the rails: the rules, the messaging standards, and the infrastructure that connects issuers and acquirers. Think of them as the telephone network connecting two banks. For providing this network, they charge their own fee, called the scheme fee or assessment fee, typically about 0.13% to 0.15% of the transaction value (Visa USA Interchange Reimbursement Fees, April 2026).

Follow the money: what happens to your $100

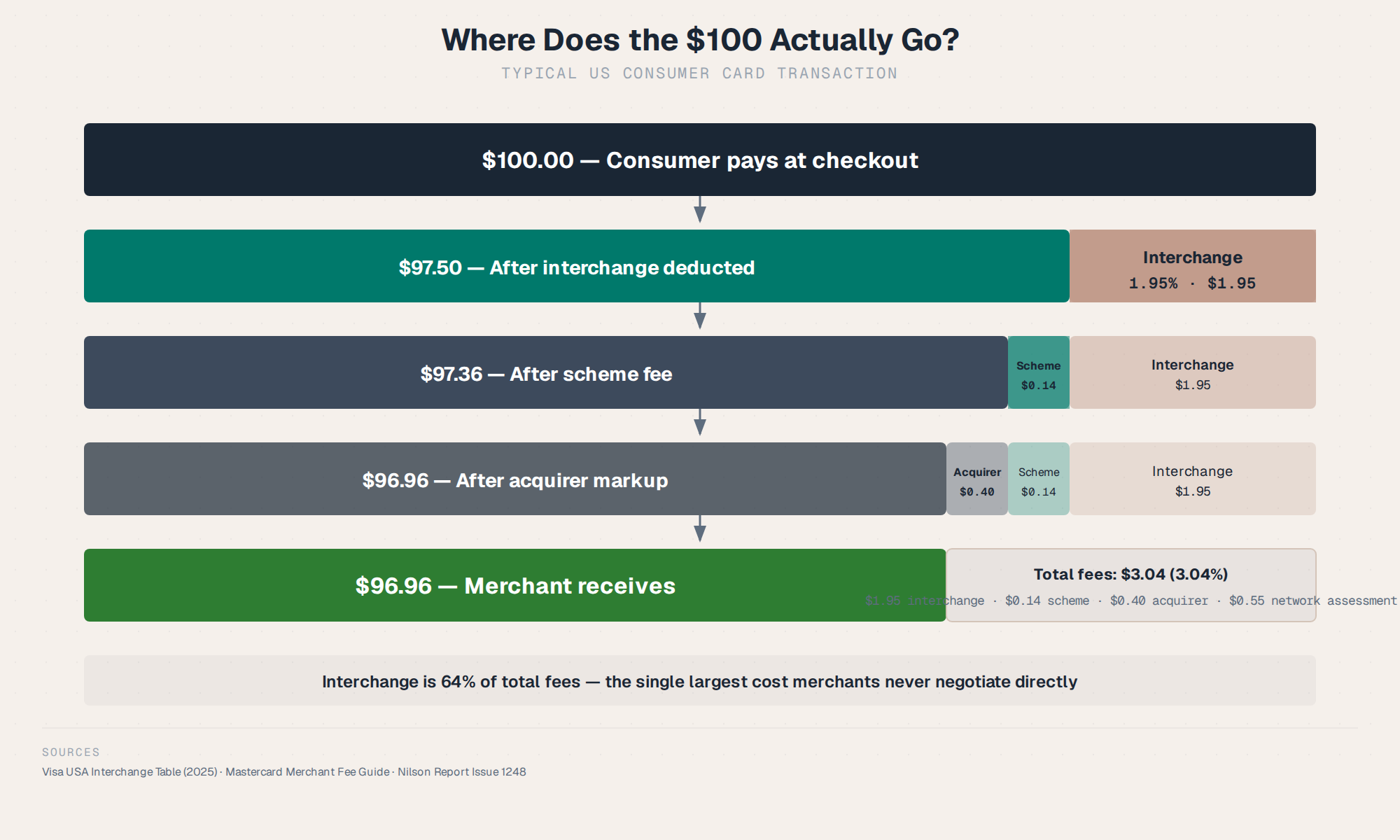

Let's trace a $100 credit card payment in the US, step by step.

You tap your card for $100. The merchant's terminal sends an authorization request through the acquirer, across the Visa or Mastercard network, to your bank (the issuer). Your bank checks: do you have credit available? Is this transaction suspicious? If everything looks right, it sends back an approval. The money is authorized but not yet settled.

A day or two later, settlement happens. The money actually moves. Here's where the fees come out.

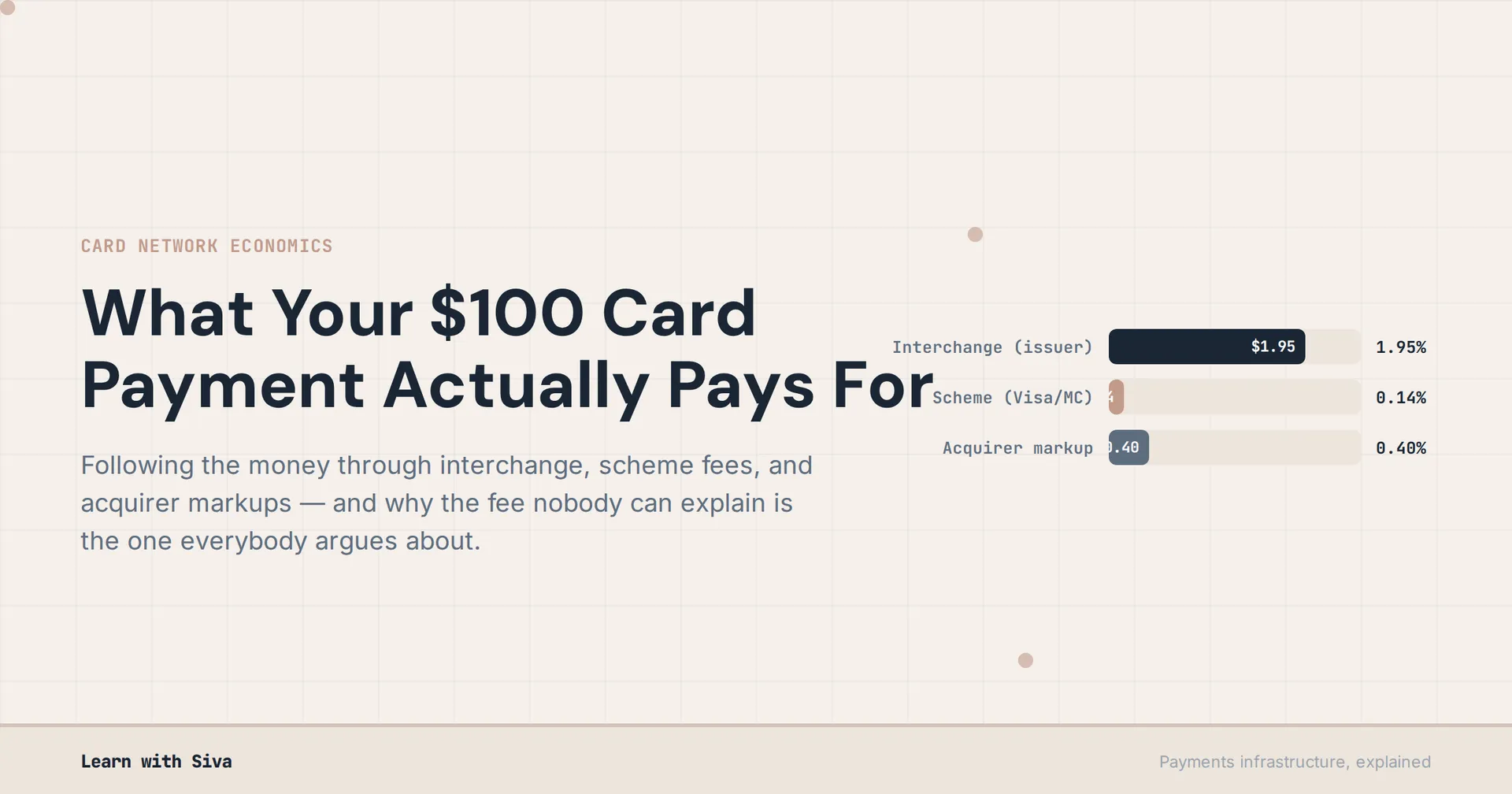

The merchant does not receive $100. The total fee the merchant pays is called the Merchant Discount Rate (MDR), and it's typically 1.5% to 3.5% of the transaction, depending on the country and card type (SingSaver, December 2025). For a US credit card transaction at roughly 2.5% MDR, here's the breakdown:

- Interchange fee (to the issuer): approximately $1.95. This is the largest single fee, representing about 70% to 90% of the total MDR (Wikipedia: Interchange Fee).

- Scheme/assessment fee (to Visa/Mastercard): approximately $0.14, or about 0.14% (Mastercard Merchant Interchange Rates).

- Acquirer markup (to Stripe, Adyen, etc.): approximately $0.40, or about 0.40%.

That leaves the merchant with about $97.51 out of the original $100.

The key insight: interchange is not a fee the merchant pays directly. The acquirer pays interchange to the issuer, and the acquirer recovers it (plus its own markup) from the merchant through the MDR. The merchant never sees the interchange line item unless they're on an interchange-plus pricing model.

Why interchange exists: the chicken-and-egg problem

Card networks have a problem that most businesses don't. They need two groups of customers at the same time: consumers who carry cards, and merchants who accept them. Without merchants, consumers won't carry cards. Without consumers, merchants won't install card terminals.

Economists Jean-Charles Rochet and Jean Tirole formalized this as two-sided market theory in a series of papers published in 2003 and 2004 (Rochet & Tirole, "Platform Competition in Two-Sided Markets," JSTOR, 2003). Their insight: in a two-sided market, the platform doesn't charge both sides equally. It charges the side that's less price-sensitive more, and subsidizes the side that's harder to attract.

In payments, that means the cardholder gets a good deal (rewards, zero liability, interest-free periods), and the merchant pays for it through interchange. This isn't an accident. It's the economic architecture that made card networks viable in the first place.

Back in the 1960s, when Bank of America launched the BankAmericard program (which later became Visa), banks needed a way to convince other banks to issue cards and merchants to accept them. The interchange fee, paid from the merchant's bank to the cardholder's bank, was the incentive. Banks got revenue for issuing cards. Merchants got access to card-carrying customers (Federal Reserve History: Electronic Point-of-Sale Payments).

That incentive structure is still in place today.

What interchange actually funds

This is the part most people skip. Interchange revenue doesn't just sit in the issuer's pocket. It funds a stack of services that cardholders and merchants rely on.

Fraud detection and zero-liability protection. When your card is stolen and someone uses it, you're not liable for those charges. Your bank eats the cost. In 2024, payment card fraud losses globally exceeded $40 billion. Interchange helps issuers absorb those losses and invest in fraud detection systems like Visa's Advanced Authorization and Mastercard's Decision Intelligence (Mastercard Australia: Interchange).

Rewards programs. Cashback, airline miles, points. These aren't free. They're funded largely by interchange revenue. When interchange is capped, rewards programs shrink. That's exactly what happened in Europe after the EU capped interchange in 2015.

Network security infrastructure. EMV chip technology (named after Europay, Mastercard, and Visa, the three companies that created the standard), tokenization (replacing your actual card number with a virtual one for mobile wallets), and 3D Secure (the extra authentication step for online purchases) are all maintained and upgraded using revenue that flows through the interchange system.

Credit risk. When you use a credit card, the issuer lends you money for up to 55 days interest-free. That's not free money for the bank. It's a loan with a grace period. Interchange helps offset the cost of extending that credit.

Customer service. The 24/7 fraud hotline, the dispute resolution process, the replacement card shipped overnight when you lose yours abroad. These operations cost money, and interchange helps pay for them.

Industry estimates suggest the rough allocation of interchange revenue looks something like this: rewards programs take about 40 to 45%, fraud losses and prevention about 15 to 20%, funding costs (that interest-free period) another 15 to 20%, network and processing operations 10 to 15%, customer service and other costs 5 to 10%, with the issuer's actual net margin at roughly 5 to 10% (Clearly Payments: Future of Interchange Fees, 2026). These are estimates. Issuers don't publicly disclose the exact breakdown.

The complexity problem: 300+ rate categories

Here's where things get messy. There isn't one interchange rate. There are hundreds.

Visa and Mastercard each maintain hundreds of interchange rate categories. The rate you pay depends on: what type of card was used (credit, debit, prepaid, commercial), what kind of merchant is accepting it (supermarket, gas station, online retailer, hotel), how the transaction was processed (card present with chip, contactless tap, online with no physical card), the transaction amount, whether the card was tokenized, the region of the issuing bank, and how quickly the transaction was settled (Adyen: Interchange Fees Explained, April 2026).

A single merchant's monthly processing statement can include dozens of different interchange rates. Most merchants don't understand their own statements. Many acquirers offer "blended" pricing, which bundles interchange, scheme fees, and acquirer markup into a single rate, making it impossible for the merchant to see what's actually going to the issuer versus the network versus the acquirer.

This opacity is the real problem. Not the fee itself, but the fact that nobody, not the merchant, not the regulator, and often not even the acquiring bank's account manager, can clearly explain the pricing structure to the merchant.

The global patchwork: same cards, different rules

One of the strangest things about interchange is how much it varies by region, even though the card networks are global.

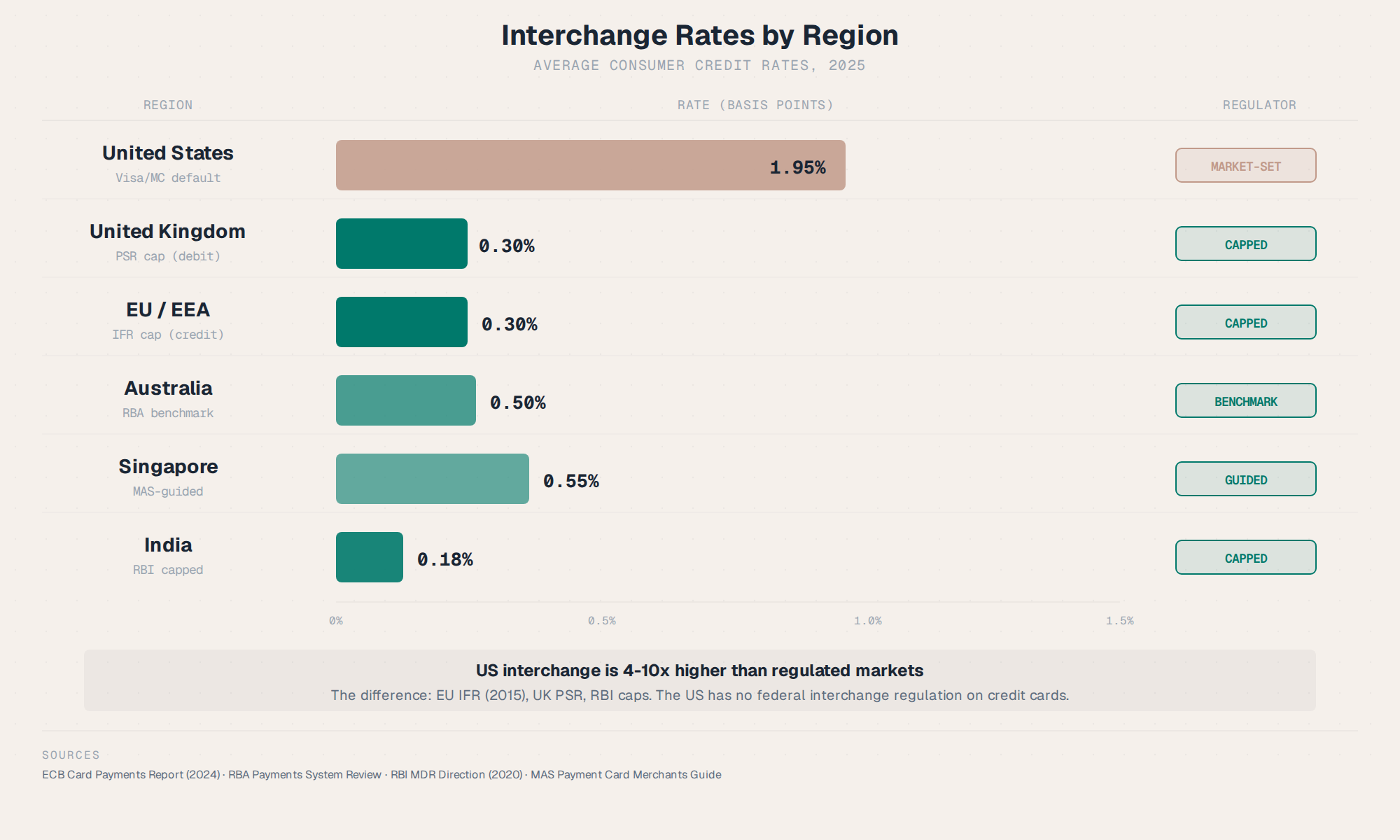

United States: Credit card interchange averages about 1.95% to 2.40%, uncapped. Debit interchange for large issuers (those with over $10 billion in assets) is capped by the Durbin Amendment at $0.21 plus 0.05% per transaction, with a $0.01 fraud-prevention adjustment for eligible issuers (Federal Reserve Regulation II). For a $100 debit transaction, that's $0.26 maximum. But here's the twist: for small-ticket transactions under about $10, the old percentage-based rate was actually lower than the Durbin cap. So capping interchange increased the cost of small debit transactions.

European Union: Since 2015, the EU Interchange Fee Regulation (IFR) has capped interchange at 0.2% for debit cards and 0.3% for credit cards (EUR-Lex Regulation 2015/751). That's roughly one-seventh the US credit rate. The result: interchange revenue for European issuers dropped significantly. Issuers responded by cutting rewards, introducing annual fees, and scaling back benefits. The fee didn't disappear. It shifted.

United Kingdom: The UK mirrors EU caps at 0.2% (debit) and 0.3% (credit), regulated by the Payment Systems Regulator (UK PSR: The IFR). Post-Brexit, UK-to-EEA cross-border interchange rates rose to 1.15% for debit and 1.5% for credit, a case study in what happens when regulatory alignment ends (Clearly Payments, October 2025).

Singapore: No interchange regulation. Rates are set entirely by card networks. The total MDR ranges from 1.5% to 3.5%, with interchange making up the largest portion (Airwallex SG: Interchange Fees in Singapore, June 2024). PayNow, Singapore's instant payment system, offers zero merchant fees for QR-based payments, creating a real alternative for small merchants.

Australia: The Reserve Bank of Australia (RBA) has capped interchange since 2003, with credit card rates around 0.50% to 0.55%. Australia was the first major economy to regulate interchange.

Canada: Interchange was reduced through voluntary agreements between the federal government and card networks, with credit rates around 1.40% generally and 0.95% for small businesses.

What happens when you cap interchange

The EU and Australia have run the experiment. The results are consistent, and they're not what most people expect.

When interchange is capped, the fee doesn't vanish. It moves. Issuers make up the lost revenue through other channels: higher annual card fees, reduced rewards, higher interest rates on revolving balances, and fewer zero-fee card offerings. In some cases, issuers scale back fraud prevention investments because they no longer have the revenue to fund them.

After the Durbin Amendment in the US, something similar happened. Debit interchange revenue for covered issuers dropped. But merchant acquiring margins actually grew. The savings didn't fully pass through to merchants. Some of the gap was captured by acquirers and processors (Philadelphia Fed Working Paper WP25-18, 2025).

The Durbin Amendment also had an unintended consequence for small-ticket purchases. The $0.21 flat component of the cap made small transactions more expensive. A $4 coffee that previously cost $0.04 in interchange (at a 1% rate) now costs $0.21. That's a five-fold increase.

The lesson: capping interchange is a price control on one input. It doesn't control the total cost to the merchant or the consumer. It changes who captures the margin.

2026: the year interchange went to court

Three things happened in quick succession in 2025 and 2026 that made interchange a mainstream regulatory issue in the US.

First, Illinois passed the Interchange Fee Prohibition Act (IFPA) in 2025. The law would have prohibited merchants from being charged interchange on the tax and tip portions of card transactions. The logic was straightforward: if sales tax isn't revenue for the merchant, why should the merchant pay a fee on it?

In April 2026, the Office of the Comptroller of the Currency (OCC) issued an interim final rule preempting the Illinois IFPA for nationally chartered banks (Federal Register, April 29, 2026). The OCC's position: states cannot regulate the fees charged by national banks, and interchange is a fee set at the network level, not the state level. The Seventh Circuit also vacated the district court's preliminary injunction, adding another layer of legal complexity (JD Supra: OCC Preempts Illinois IFPA, April 2026).

Second, Visa and Mastercard proposed a revised $38 billion settlement with US merchants who accused the card networks of charging excessive interchange fees. A federal judge reviewed the settlement in April 2026. Walmart and other large merchants objected, arguing the amount was insufficient. The judge warned critics that a trial might not deliver better outcomes (Reuters, April 27, 2026). In May 2026, the Second Circuit rejected an attempt to narrowly construe a prior settlement agreement (NY Law Journal, May 20, 2026).

Third, the Federal Reserve proposed expanding Regulation II to enhance competition in debit routing. Currently, merchants can route debit transactions through different networks (not just Visa/Mastercard), but the rules around which networks qualify and how they're enabled are complex. The proposed changes would make it easier for merchants to choose lower-cost routing options (Federal Register, November 2023).

These three threads, state preemption, class action settlements, and routing competition, are converging. Interchange regulation in the US is not a question of "if" but "how."

The real question isn't "how much." It's "can anyone explain this?"

Everyone argues about whether interchange is too high. The US charges roughly 2% for credit. The EU charges 0.3%. Same cards. Same networks.

But the real scandal isn't the rate. It's the opacity.

Interchange has over 300 rate categories. Most merchants cannot read their own processing statements. Blended pricing models hide interchange behind a single rate. Interchange-plus models expose it but require a degree in payments infrastructure to interpret.

The merchants who argue interchange is too high are right that the pricing is opaque. The issuers who argue interchange funds critical services are right that caps shift costs, not eliminate them. The regulators who cap interchange are right that market forces alone haven't produced transparent pricing.

They're all talking past each other because they're arguing about the wrong thing.

The question isn't whether interchange should be 2% or 0.3%. The question is: in a system that processes trillions of dollars annually, why is the largest single fee still something most participants cannot clearly explain?

What does this mean for Singapore?

Singapore sits in an unusual position. MAS (the Monetary Authority of Singapore) has not regulated interchange fees. The card networks set rates, and the MDR ranges from 1.5% to 3.5% (Airwallex SG; Eats365 SG, January 2026).

But Singapore also has PayNow, an instant payment system that offers zero-cost QR-based payments for merchants. For small businesses, PayNow is a genuine alternative to card acceptance. The SGQR initiative, which consolidates multiple payment QR codes into one, makes it even easier.

The question for Singapore is whether market competition from instant payments will do what regulation has done elsewhere: push down the effective cost of card acceptance. Or whether interchange remains stubbornly high because consumers prefer cards for the rewards, and merchants can't afford to refuse cards.

That tension, between a free instant payment rail and a costly but rewards-rich card rail, is playing out in real time across Southeast Asia.

The trade-off

Interchange is not a tax. It's not a subsidy. It's the price of a payment system where the cardholder gets rewards, fraud protection, and interest-free credit, and the merchant gets guaranteed payment and access to card-carrying customers.

That price is high in some markets and low in others. Capping it doesn't eliminate it. It moves it to annual fees, higher interest, or weaker fraud protection.

The real problem is that most participants in the system, merchants, consumers, and even many bankers, cannot explain the fee they're paying or receiving. That's not a pricing problem. That's a transparency problem.

And transparency problems don't get solved by price caps. They get solved by making the pricing legible.

Sources

- Federal Reserve Regulation II Average Interchange Fee: federalreserve.gov

- EUR-Lex Regulation 2015/751 (EU IFR): eur-lex.europa.eu

- UK PSR The IFR: psr.org.uk

- Federal Register Debit Card Interchange (Nov 2023): federalregister.gov

- OCC Order Preempting Illinois IFPA (Apr 2026): federalregister.gov

- Visa USA Interchange Reimbursement Fees (Apr 2026): usa.visa.com

- Mastercard Merchant Interchange Rates: mastercard.com

- Philadelphia Fed WP25-18 (2025): philadelphiafed.org

- Clearly Payments Future of Interchange (Oct 2025): clearlypayments.com

- Adyen Interchange Fees Explained (Apr 2026): adyen.com

- Airwallex SG Interchange Fees (Jun 2024): airwallex.com

- SingSaver SG Credit Card Processing (Dec 2025): singsaver.com.sg

- ChargebackGurus Understanding MDR: chargebackgurus.com

- Eats365 SG Reduce MDR (Jan 2026): eats365pos.com

- Motley Fool Avg Processing Fees 2025: fool.com

- Financial Professionals Interchange Glossary: financialprofessionals.org

- Reuters Visa/MC $38B Settlement (Apr 2026): reuters.com

- JD Supra OCC Preempts Illinois IFPA (Apr 2026): jdsupra.com

- American Banker OCC Preempts Illinois (Apr 2026): americanbanker.com

- NY Law Journal Second Circuit Ruling (May 2026): law.com

- Rochet & Tirole Two-Sided Markets (JSTOR, 2003): jstor.org

- Federal Reserve History Electronic POS Payments: federalreservehistory.org

- Wikipedia Interchange Fee: en.wikipedia.org

- Mastercard Australia Interchange: mastercard.com.au