The Three Forms of Digital Money: What's Actually Live, What's Still Theory, and Where the Money Is Moving

The Three Forms of Digital Money: What's Actually Live, What's Still Theory, and Where the Money Is Moving

Tokenised deposits are the quiet frontrunner in institutional digital money. Not stablecoins. Not CBDCs. Tokenised deposits. And the gap between hype and deployment is wider than most people think.

JP Morgan's Kinexys platform has processed over $2 trillion in notional value. $3 billion moves through it daily. That is not a pilot. That is core settlement infrastructure running on blockchain rails, operated by one of the world's largest banks for institutional clients, several years running.

Meanwhile, the conversation about digital money still orbits stablecoin drama and CBDC speculation. Neither of those is wrong. Both are real. But if you want to understand where institutional money is actually going right now, you need to look at the three forms of digital money side by side: stablecoins, tokenised deposits, and central bank digital currencies. What each one does. Where each one works. And what the banks routing between them are thinking.

This piece builds on Deutsche Bank's 2026 white paper "Digital Money: A Perspective on Stablecoins, Tokenised Deposits and CBDCs" and extends it with production data from the platforms actually running.

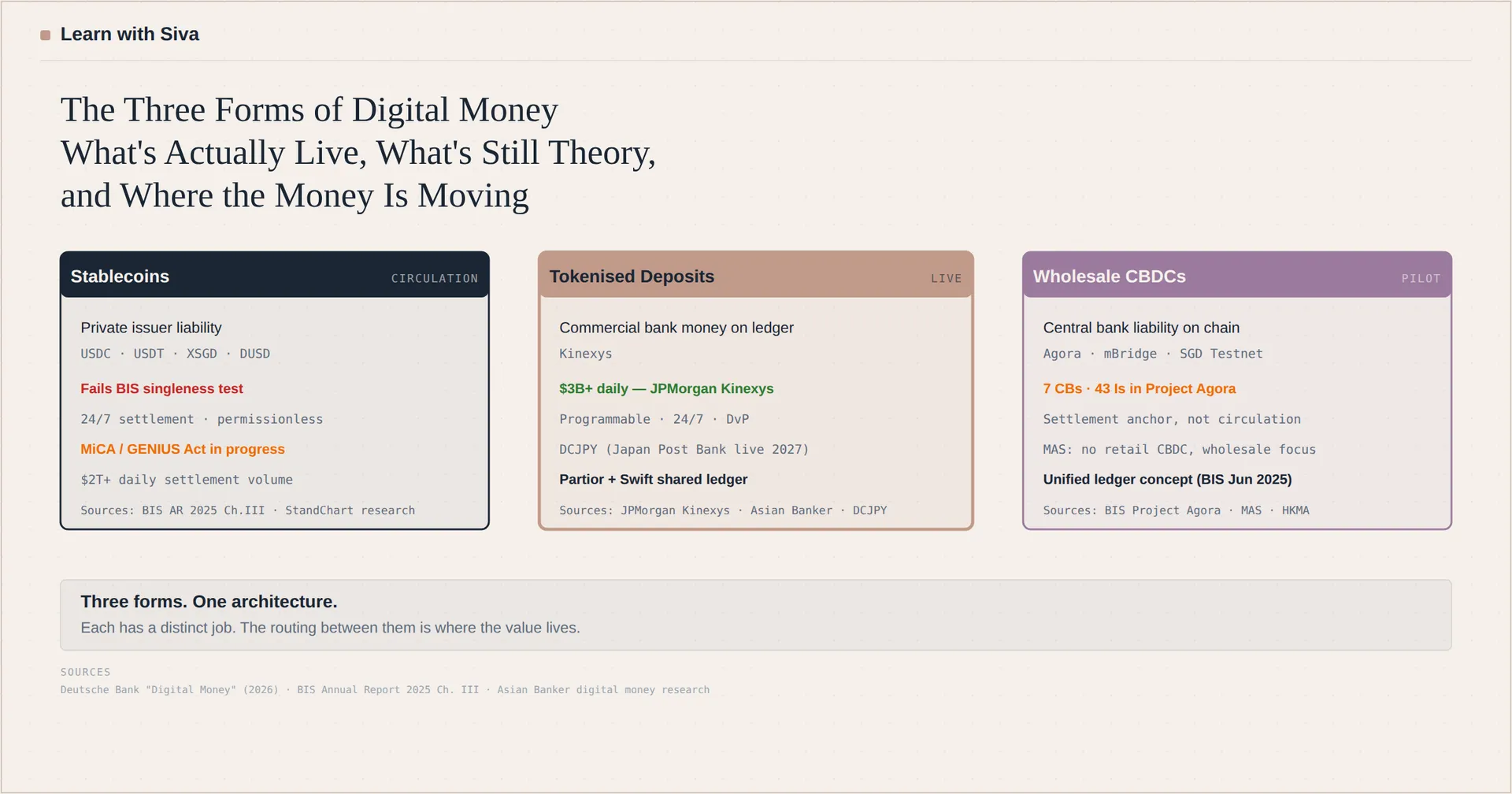

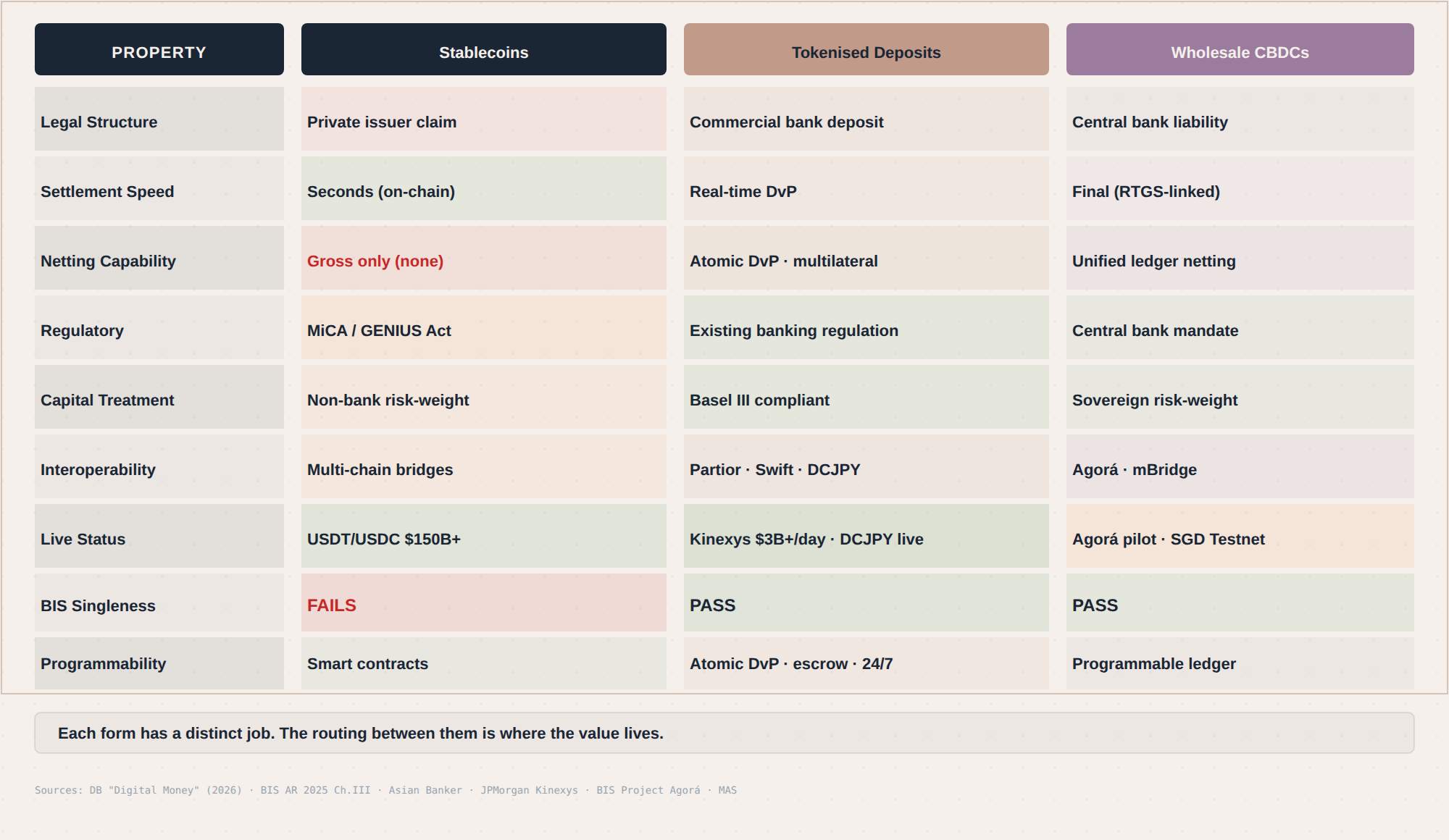

Stablecoins: Fast Money, Uneven Foundation

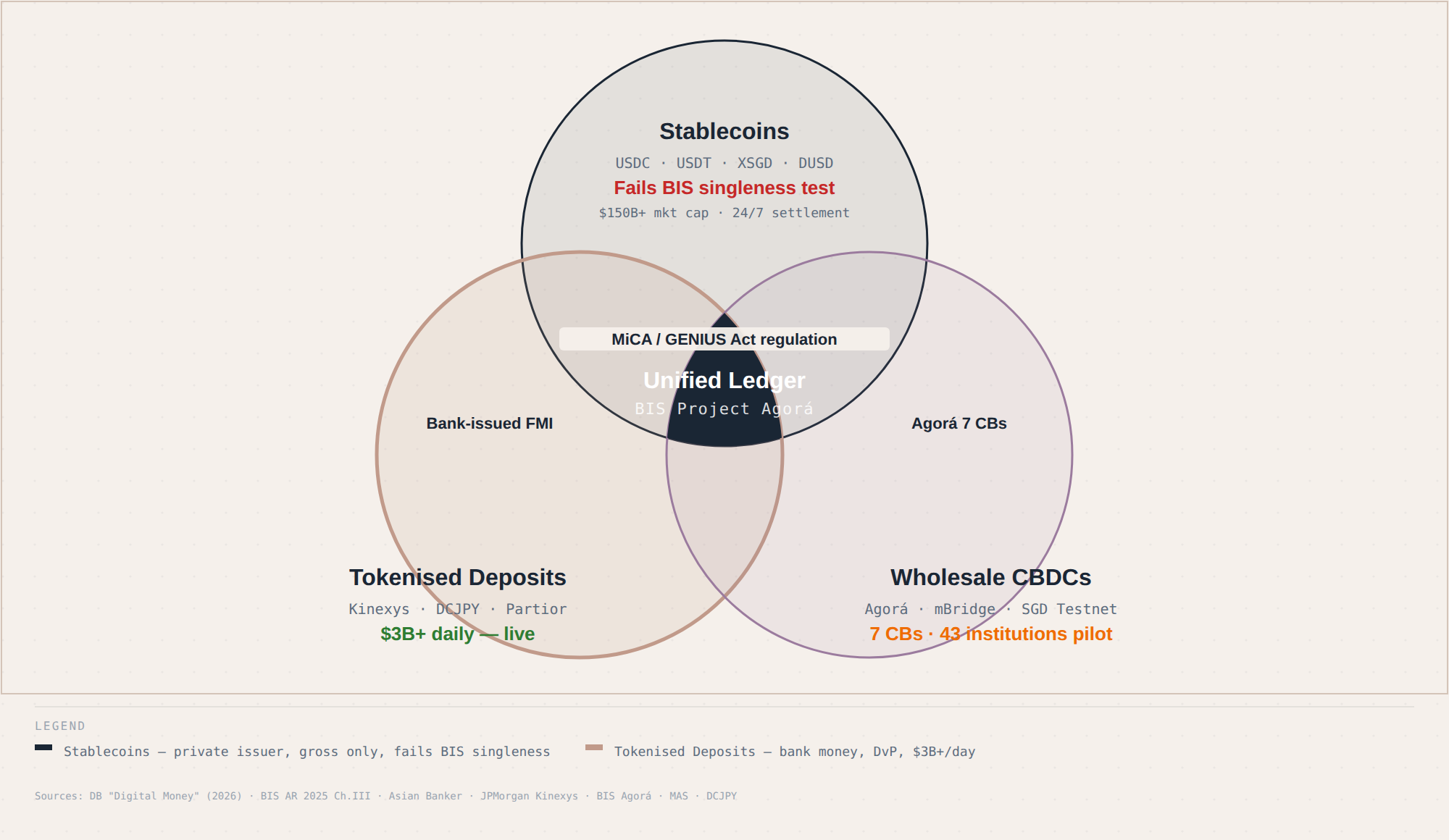

Stablecoins do one thing well: they move fast on permissionless infrastructure. Circle's USDC and Tether's USDT settle in seconds on public blockchains. StraitsX's XSGD enables Grab and Alipay+ transactions with instant settlement and reduced foreign exchange exposure. Paolo Ardoino, CEO of Tether, describes stablecoins as "recognised as powerful technology" with adoption across emerging markets.

That speed matters. In cross-border corridors where correspondent banking introduces multi-day delays and FX risk, a stablecoin that settles in seconds has real utility. Geoffrey Kendrick, global head of digital assets research at Standard Chartered, projects significant growth in stablecoin market capitalisation if regulatory regimes like MiCA (EU), the GENIUS Act (US), and frameworks in Hong Kong and Singapore provide consistent treatment.

But speed is not the same as sound money.

The Bank for International Settlements applies three tests to any form of money: singleness (one unit always equals one unit), elasticity (supply adjusts to demand), and integrity (governance prevents misuse). Stablecoins fail the singleness test. USDC and USDT trade at slightly different rates. Different issuers hold different reserve compositions. In stress events, some stablecoins have depegged. The BIS compares this to 19th century private banknotes: multiple issuers, varying redemption quality, no guarantee that one unit from Issuer A equals one unit from Issuer B.

This does not make stablecoins useless. It makes them a circulation layer, not a settlement anchor. Jack McDonald at Ripple argues that bank-issued stablecoins "can be considered extensions of the banking system governed by strict safeguards like capital requirements and redemption rights." That framing is accurate for regulated stablecoins. But the label does not change the underlying structural issue: stablecoins are a liability of a private issuer, not a claim on the banking system or the central bank.

For institutional use, that matters. Banks need to know that settlement is final, that the asset will hold its value through the settlement window, and that the legal framework around it is clear. Stablecoins are getting there in some jurisdictions. They are not there yet in most.

Tokenised Deposits: The One Banks Are Actually Deploying

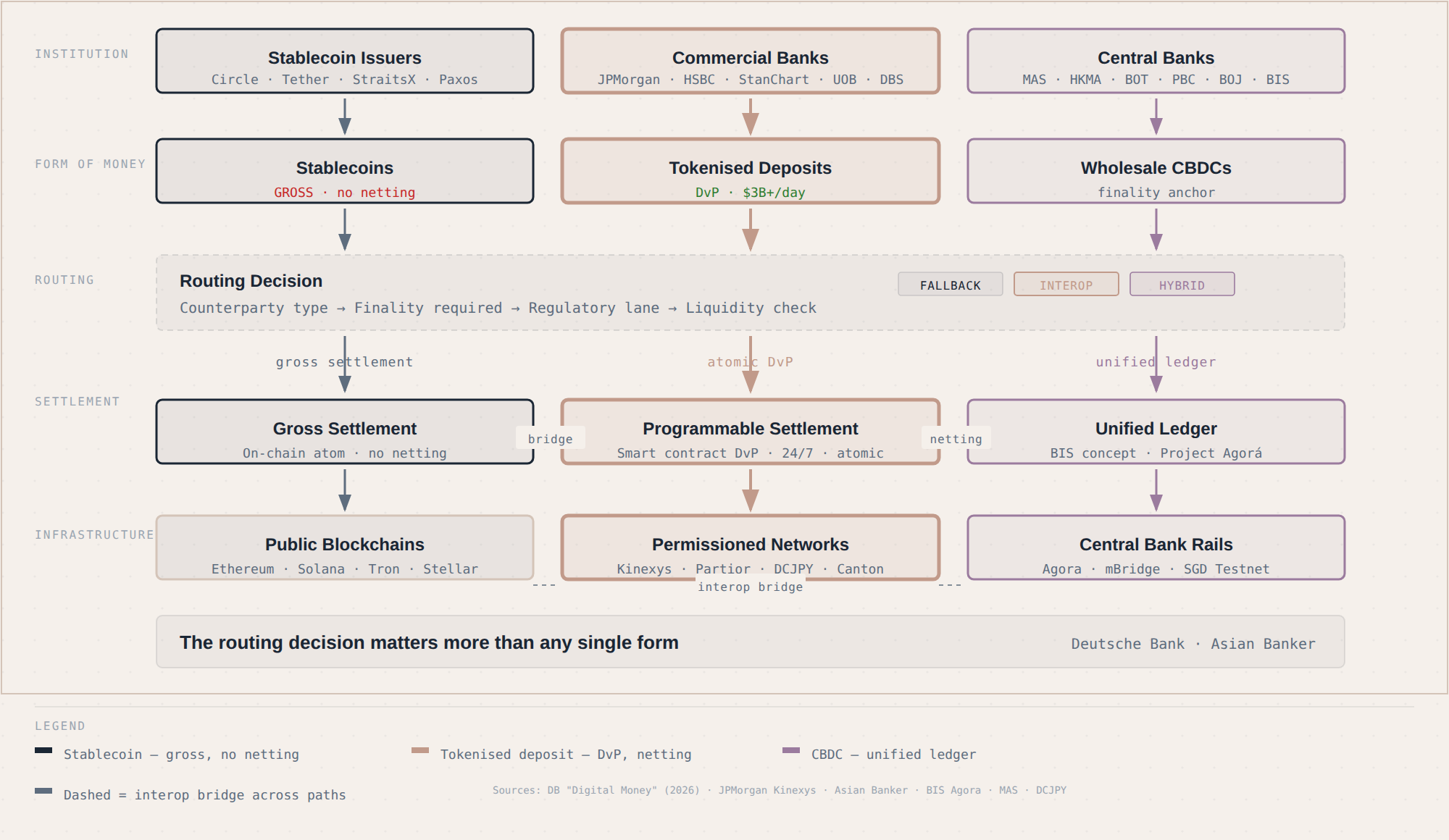

Tokenised deposits are commercial bank money placed on ledger infrastructure. The deposit is the same legal instrument it has always been. The difference is the rails it runs on.

This is the most advanced format for commercial banks because it requires no legal change to the nature of the deposit. The bank still owes the depositor. The depositor still has the same claim. But the deposit can now move on a programmable, 24/7 settlement layer with smart contract logic embedded in the transaction flow.

JP Morgan's Kinexys is the clearest example. Akshika Gupta, global head of client solutions for Kinexys, confirmed the platform processes "more than $3 billion in daily transaction volume" across post-trade and on-chain cash. This is not a sandbox. It is settlement infrastructure.

Standard Chartered and HSBC have launched institutional settlement pilots in Hong Kong reflecting the same logic: put commercial bank money on chain, keep the legal deposit unchanged, add programmability. Manuel Klein, head of market management for payments and digital currencies at Deutsche Bank, describes Partior and Swift's shared ledger as "complementary expressions of the same architectural shift: moving commercial bank money onto ledger infrastructure without fragmenting liquidity or governance."

Japan offers a blueprint for interoperability. DCJPY is a regulated, multi-issuer tokenised deposit platform where participating banks issue interoperable tokens under a shared framework. Mai Kaneko from DeCurret DCP confirmed that "the first issuing bank is already live, and Japan Post Bank is expected to become the second issuing bank next year." She emphasised that "there is one DCJPY and it is fully interoperable between banks," enabled by standardised smart contracts and common issuance and redemption rules.

This interoperability question is the real constraint. Kara Kennedy, global co-head of Kinexys at JP Morgan, described the current state as "islands of innovation." David Katz from Circle observed that "Bank B may not accept Bank A's tokenised deposit," creating what he called "walled gardens." These isolated networks limit liquidity mobility even where individual platforms function reliably. Banks acknowledge they are heading toward a "multi-chain, multi-solution end state."

The walled garden problem is not trivial. If Bank A issues a tokenised deposit on its own ledger and Bank B issues on a different ledger, moving value between them requires either a bridge (with counterparty risk), a common settlement layer (which is what Swift and Partior are building), or bilateral agreements that recreate the correspondent banking model in new wrapping.

CBDCs: The Settlement Anchor

Wholesale CBDCs serve a different function. They are a direct liability of the central bank, sitting on a tokenised platform. They do not replace tokenised deposits or stablecoins. They settle them.

When two banks move tokenised deposits against each other, the question of what settles the net position remains. In traditional correspondent banking, that settlement happens through nostro and vostro accounts, RTGS systems, or correspondent clearing. On tokenised platforms, wholesale CBDC provides a settlement asset with central bank backing, giving the transaction legal finality.

Project Agorá, coordinated by the BIS, brings together seven central banks and 43 financial institutions to test exactly this. The prototype explores how tokenised commercial bank money and tokenised central bank money can coexist on the same programmable platform. The BIS calls this the "unified ledger" concept: one platform carrying tokenised central bank reserves, commercial bank deposits, and government bonds, settled atomically.

The Monetary Authority of Singapore has stated it has no plans to issue a retail CBDC. Its focus is wholesale. The SGD Testnet supports legally final interbank settlement in live environments. Project Guardian tests tokenised asset use cases. BLOOM, an MAS industry pilot, explores multi-currency digital settlement infrastructure. Hong Kong's Project Ensemble and the Virtual Asset Trading Platform regime pursue similar wholesale objectives.

These programmes are not small. But they are also not yet running at the scale of Kinexys. CBDC programmes advance at different speeds because central banks optimise for different domestic priorities. The point is not which is fastest. The point is what role CBDCs play in the architecture: they are the settlement anchor, not the circulation layer.

Liu Tianwei, co-founder and CEO of StraitsX, described the relationship clearly: "Tokenised deposits act like private ledgers within a bank's ecosystem. Stablecoins function more like e-money: open, efficient, and suitable for a wide range of applications." Most central banks, he noted, expect CBDCs to remain wholesale instruments. The triangle is deliberate: each form has a job.

The Architecture Taking Shape

Three observations from the production data and the people running these platforms.

First, the hybrid model is the model. Rene Michau, group head of digital assets at Standard Chartered, argued that "public blockchains represent a new operating system for financial services that can coexist with, rather than replace, traditional rails." Lee Zhu Kuang at UOB described structures where "assets such as money market funds may be issued on public chains, while certification, custody and control operate on private chains." Banks are not ripping out RTGS, correspondent banking, or Swift messaging. They are adding tokenised rails alongside them.

Second, the routing decision matters more than any single form. Deutsche Bank's white paper makes the point clearly: banks will abstract complexity by routing each transaction to the form of money that fits. A cross-border wholesale payment might route through tokenised deposits on Partior, settled against wholesale CBDC. A retail remittance might use a regulated stablecoin for speed and reach. The bank makes the call, not the end user. John O'Neill, group head of digital assets and currencies at HSBC, put it plainly: "The future system is supported by tokenised deposits, CBDCs and regulated stablecoins. We follow our clients wherever the demand is."

Third, interoperability is the bottleneck, not technology. The platforms work. Kinexys processes billions daily. Partior settles atomically in production. The question is how to move liquidity across these platforms without recreating the fragmentation that tokenised rails were supposed to solve. Swift's shared ledger approach, confirmed by CEO Javier Perez-Tasso, sits alongside existing messaging and allows tokenised deposits and on-chain money to be referenced, synchronised, and settled while preserving correspondent relationships and ISO 20022 standards. Partior provides the bank-governed network layer. These are complementary, not competing, responses to the same problem.

Operational Risks That Do Not Go Away

Programmable settlement introduces risks that banks manage directly.

Key dependency is one. Lose the cryptographic key, lose the asset. There is no help desk. Danielle Szetho at Standard Chartered highlighted this directly: on public chains, "if you send assets to the wrong wallet address, you may never get them back." Smart contract governance is another. A coding error in a settlement smart contract can create a regulatory breach or a frozen position. Chan Boon Hiong from Deutsche Bank identified cybersecurity vulnerabilities and smart-contract governance gaps as emerging risks.

Liquidity remains the decisive factor. Multiple sources across the Asian Banker research identified liquidity as "the ultimate test of whether digital assets can succeed." Programmable rails that cannot attract sufficient liquidity are expensive toys.

And then there is the question of what happens when things go wrong. Lee Zhu Kuang at UOB emphasised the need for "full traceability and the ability to revert to established rails." Programmability is only useful if you can also fall back. Banks call this operational resilience. It is the same discipline they apply to every other settlement system.

Where Asia Pacific Leads

Asia Pacific has become the primary testing ground for production-grade digital money deployment. Singapore, Hong Kong, and the UAE combine advanced domestic instant payment systems with active regulatory experimentation. The MAS has no retail CBDC plans but has built wholesale infrastructure through Project Ubin, Project Guardian, BLOOM, and the SGD Testnet. Hong Kong advances through Project Ensemble and a regulated virtual asset framework. Japan has DCJPY.

The reason is straightforward. Regulators in these jurisdictions have provided enough clarity for controlled production deployment. Banks can run tokenised deposits and regulated stablecoins alongside real-time gross settlement and instant payment systems under real operating conditions. The result is not a separate digital system. It is a controlled extension of existing financial infrastructure.

Liu Tianwei at StraitsX framed the triangle clearly: tokenised deposits as bank ecosystem money, stablecoins as open e-money, CBDCs as wholesale settlement anchors. John O'Neill at HSBC: "We follow our clients wherever the demand is." Both are describing the same architecture from different vantage points.

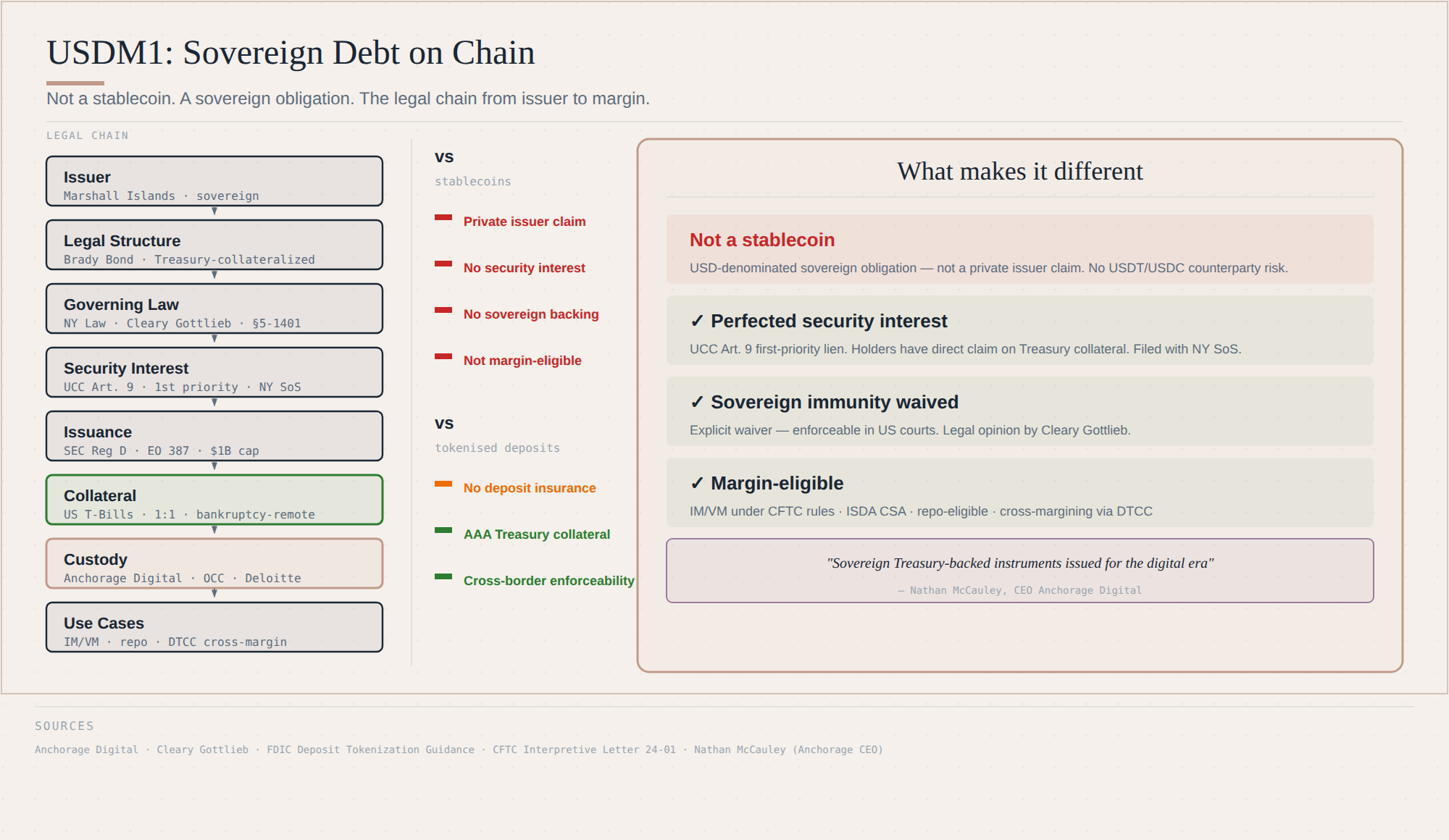

USDM1: What Happens When a Sovereign Issues on Chain

If tokenised deposits are bank money on chain, and CBDCs are central bank money on chain, USDM1 represents a third path: sovereign debt on chain. It is not a stablecoin. It is not a tokenised deposit. It is a USD-denominated sovereign obligation issued by the Republic of the Marshall Islands, backed 1:1 by U.S. Treasury instruments in bankruptcy-remote custody.

This matters because the legal treatment is materially different. Structured as a Brady bond under New York law, with Cleary Gottlieb as issuer counsel, USDM1 gives holders a perfected first priority security interest in the Treasury collateral under the UCC. The sovereign immunity waiver is explicit. Nathan McCauley, co-founder and CEO of Anchorage Digital, described it as sovereign Treasury-backed instruments issued for the digital era. Anchorage provides federally regulated custody and collateral infrastructure.

The practical implication: USDM1 can be posted as initial and variation margin in derivatives, qualifying for U.S. close-out netting protections. It fits into repo with title transfer, substitution, and reuse. It accrues a sovereign coupon while pledged. Accounting treatment aligns with sovereign debt or unrestricted cash equivalents, not digital asset exposure. This is not competing with USDC. It is competing with Treasury repo and cash collateral.

The origin story connects the dots. USDM1 was built to disburse the Marshall Islands universal basic income programme over 20 years. Hon. David Paul, RMI Minister of Finance, called it a new foundation for delivering financial services to citizens across remote atolls. The same characteristics that make it work for benefit disbursement in the Pacific (sovereign backing, 24/7 programmable settlement, legal certainty) are exactly what make it viable as institutional collateral globally.

Whether it scales depends on whether margin and collateral workflows adopt on-chain settlement. But the design is deliberate: blockchain as a settlement layer for existing capital markets instruments, not a platform for new ones.

What to Watch

The technology works. That question is settled. The questions that remain are institutional:

Will tokenised deposits achieve interoperability across bank-issued platforms, or will the "walled garden" pattern persist?

Will wholesale CBDC programmes reach the scale of commercial tokenised deposit platforms, or will they remain settlement anchors used selectively?

Will Swift's shared ledger and Partior's production network converge into a common interop layer, or will banks manage multiple bridges?

Will regulated stablecoins become a genuinely institutional settlement layer (MiCA, GENIUS Act), or will they stay in the circulation and remittance niche?

These are not technology questions. They are governance, regulatory, and commercial questions. The platforms are built. The banks are deploying. The next phase is about connecting them.

Sources

- Deutsche Bank, "Digital Money: A Perspective on Stablecoins, Tokenised Deposits and CBDCs" (2026)

- BIS Annual Economic Report 2025, Chapter III: "The Next-Generation Monetary and Financial System"

- BIS CPMI, "Tokenisation: A Review of the Literature and Risks" (October 2024)

- The Asian Banker, "Rethinking Digital Money and Settlement in a Tokenised World" (January 2026)

- Partior platform documentation and Deutsche Bank partnership announcement

- JP Morgan Kinexys production data (confirmed by Akshika Gupta, Global Head of Client Solutions)

- Swift shared ledger confirmation (Javier Perez-Tasso, CEO)

- USDM1 official documentation and Anchorage Digital partnership announcement

- Republic of the Marshall Islands Ministry of Finance