The Missing Piece in Bank Tokenized Deposits

A corporate treasurer sits at her desk on a Friday evening in Singapore. She needs to move $50 million to New York before the weekend. The SWIFT message will leave now. The actual money will settle Monday morning, US time, after the Federal Reserve's wire window reopens.

Meanwhile, a fintech startup in Buenos Aires sends a $2,000 USDC payment to a contractor in Lagos on Saturday at 11pm. It settles in 12 seconds. No bank reserve window. No correspondent chain. No waiting.

This is the gap that tokenized money is trying to close. But what "tokenized money" actually means depends entirely on who is building it, what liability sits behind the token, and whether the system can move value between different banks without falling back on the same reserve rails it was supposed to bypass.

The distinction matters more than most coverage suggests. And the hardest part of the problem, interbank settlement between tokenized deposits at different banks, does not have a production-ready solution yet.

Three forms of digital money, three different liabilities

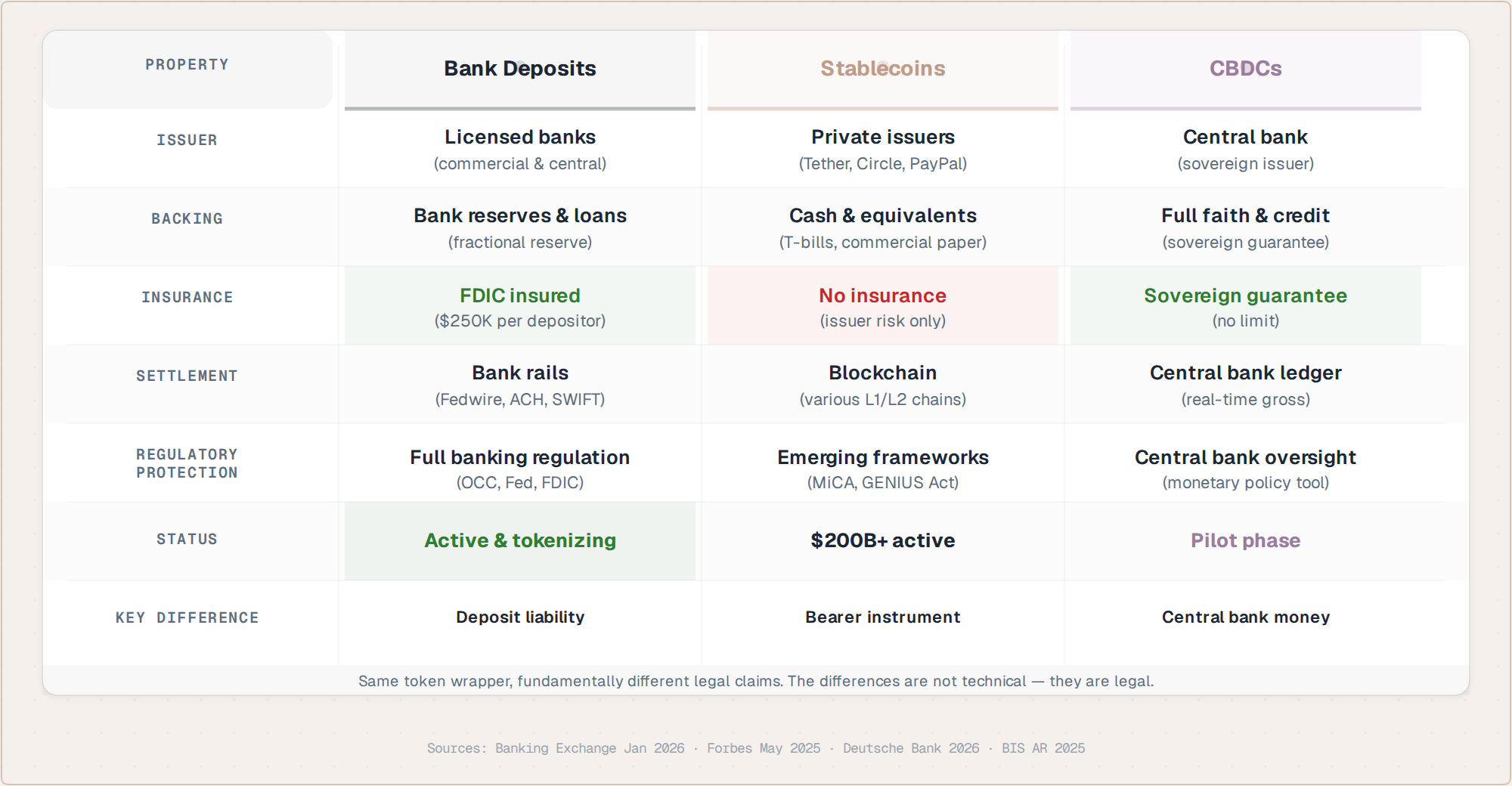

Not all digital money is the same. The differences are not technical. They are legal.

Tokenized deposits are bank deposit liabilities recorded on a blockchain. The holder has a claim on the issuing bank, exactly like a traditional deposit. That claim carries FDIC insurance up to $250,000, sits under Basel capital requirements, and has access to the Federal Reserve's lender-of-last-resort window. The bank-client relationship is preserved. As Forbes contributor Zennon Kapron put it, tokenized deposits "wrap an existing commercial-bank liability in a cryptographic shell" where "the token inherits deposit insurance, Basel capital and lender-of-last-resort support" (Forbes, May 2025).

Think of it this way: your bank balance is already a digital number on a database. A tokenized deposit makes that same number portable on a blockchain, programmable via smart contracts, and available 24/7. The underlying obligation has not changed.

Stablecoins are different. They are bearer instruments. Possession of the token equals ownership, like physical cash. USDC, USDT, and PayPal's PYUSD are backed by segregated reserves, typically short-dated US Treasuries, held in bankruptcy-remote trusts. Under the US GENIUS Act (signed July 2025), issuers must maintain those reserves and submit to regular audits (Banking Exchange, Jan 2026). But they do not carry FDIC insurance, and the holder has no claim on any bank's balance sheet.

CBDCs, or central bank digital currencies, are a third category. Retail CBDCs like China's e-CNY (which reached 14 trillion yuan, about $2 trillion, in cumulative transactions by September 2025) function as digital cash issued by the central bank itself (Deutsche Bank / FintechNews, May 2026). Wholesale CBDCs, still largely in pilot, would be the central bank equivalent of reserve balances, used for interbank settlement.

Banks are building. But what exactly?

American Banker reported in April 2026 that 19 of the top 50 US banks are developing tokenized deposit strategies, compared to 15 developing stablecoin strategies. Four are doing both (American Banker, Apr 2026).

That 19 versus 15 number has been quoted as evidence that banks are choosing one rail over the other. The reality is more layered. Banks are not choosing sides. They are building infrastructure that lets them operate on multiple rails simultaneously, because different corporate clients need different things.

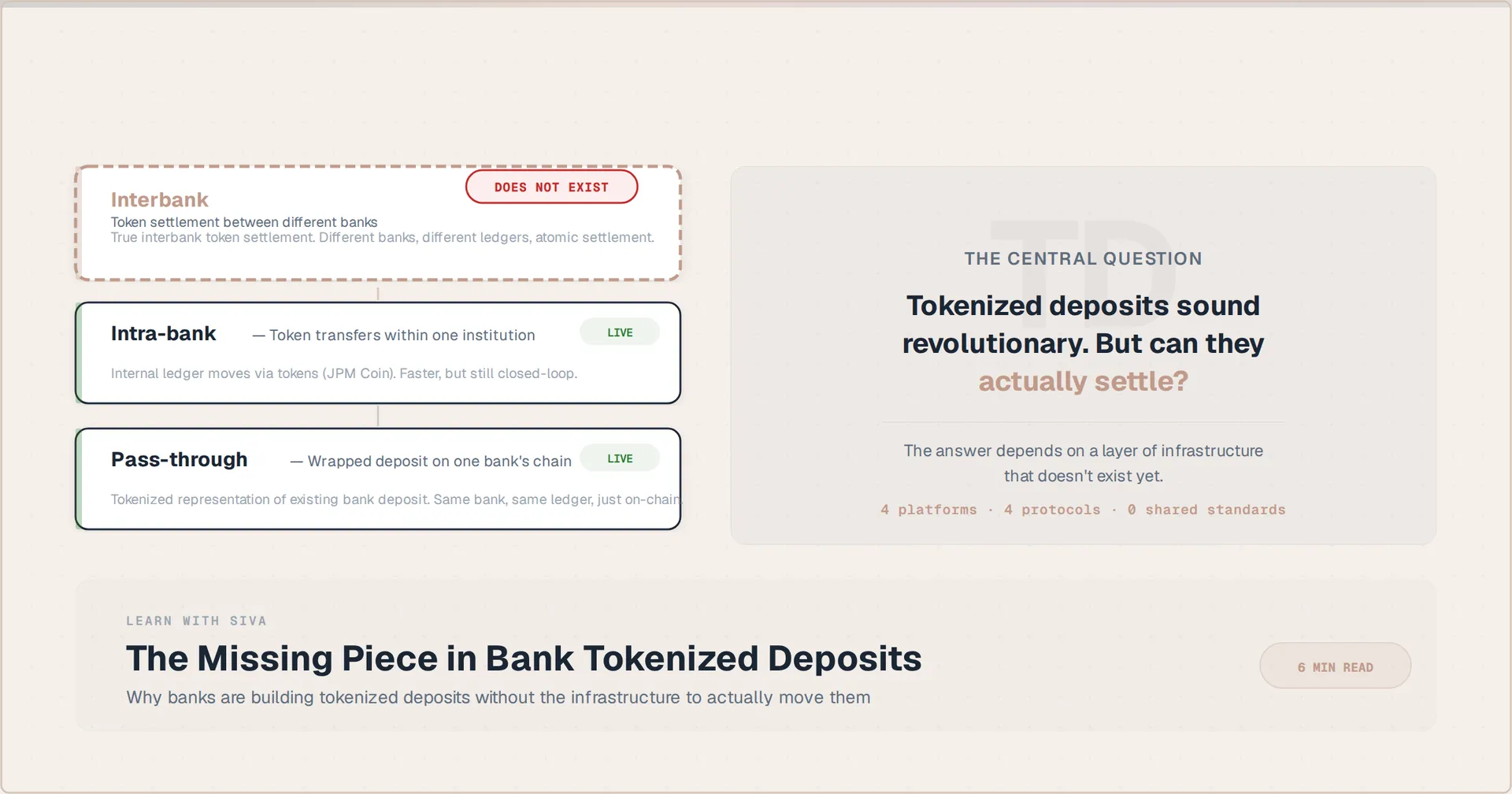

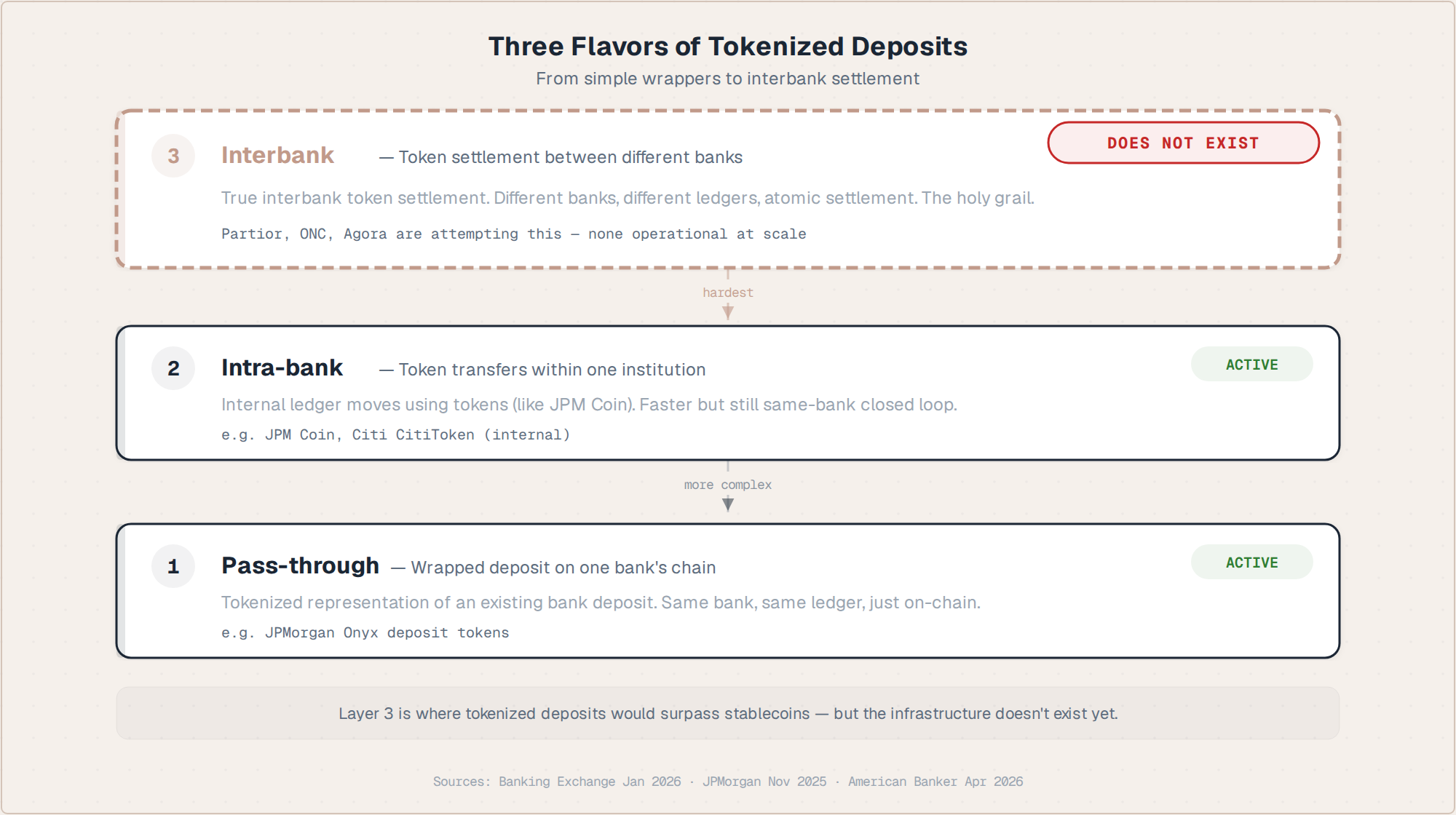

The Banking Exchange practical guide from January 2026 laid out a useful framework that most coverage misses. Tokenized deposits are not one thing. They come in three distinct models, each with very different capabilities:

Flavor 1: Intrabank settlement networks. These are systems like CUBIX, Signet, and SEN, where a single bank moves digital value between its own accounts. The blockchain element is minimal. These are essentially faster book-entry transfers, internal databases with cryptographic verification bolted on. They work within one bank's balance sheet and cannot move value to another institution.

Flavor 2: Intrabank blockchain deposits. JPMorgan's JPMD, deployed on Coinbase's Base (an Ethereum Layer 2) in November 2025, is the clearest example (JPMorgan, Nov 2025). This is a real blockchain-based deposit token, with near-instant 24/7 settlement, but it only works within JPMorgan's client base.

Flavor 3: Interbank tokenized deposits. A deposit token issued by JPMorgan could be sent to, and redeemed by, a Citi client, atomically, on-chain. As of 2026, a production-grade interbank model does not yet exist in the US market (Banking Exchange, Jan 2026).

The gap between Flavor 2 and Flavor 3 is the entire story.

The interbank gap

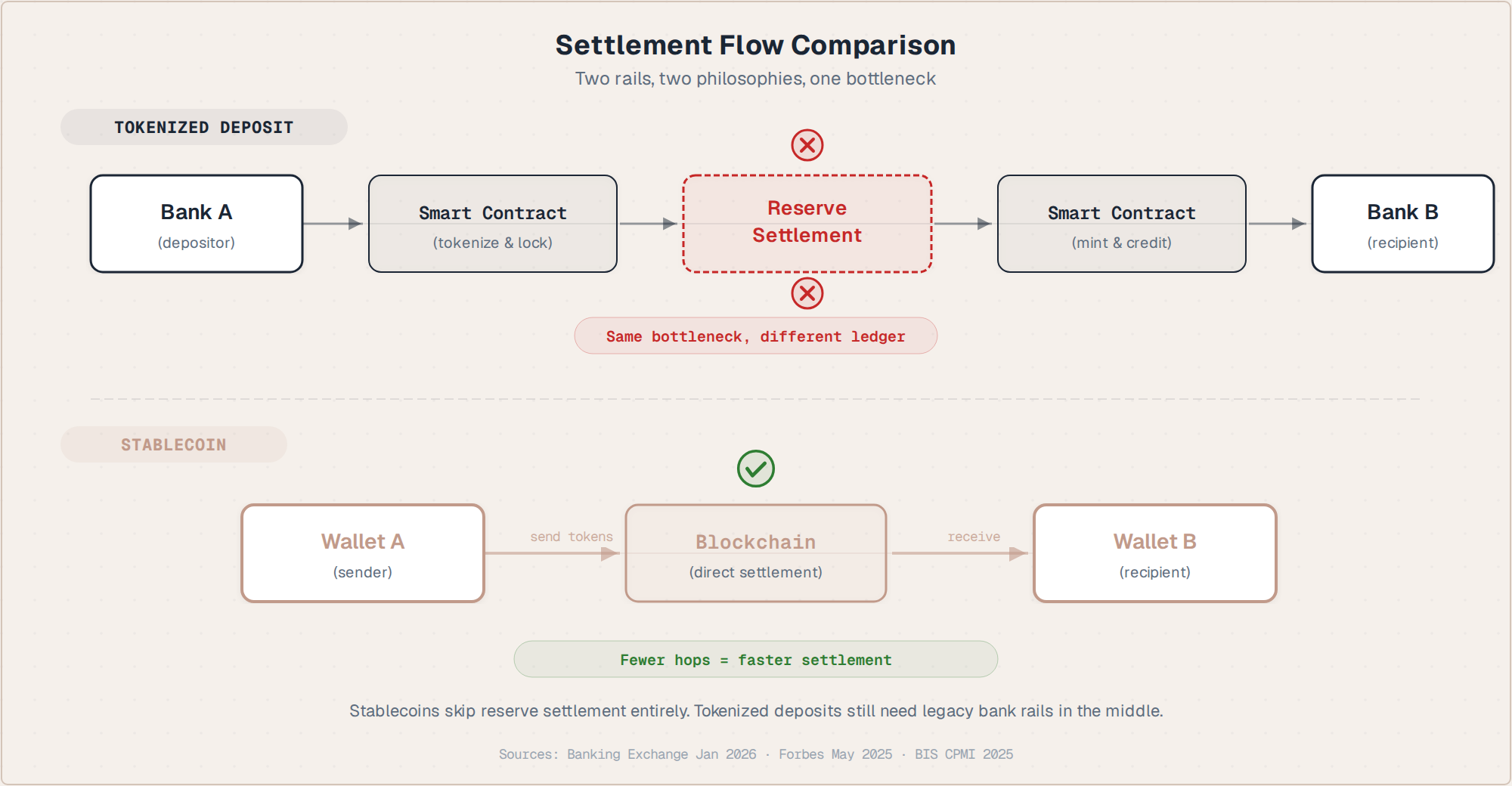

Why is interbank tokenized settlement so hard? The problem is not the blockchain. The problem is the reserve system.

When Bank A sends money to Bank B today, the actual settlement happens through the Federal Reserve's Fedwire or a clearinghouse. Bank A's reserve account at the Fed is debited. Bank B's reserve account is credited. This is settlement finality backed by the central bank.

Tokenized deposits do not bypass this. When a tokenized deposit moves from JPMorgan to Citi, the underlying liability still needs to settle through the reserve system. The blockchain makes the token transfer instant, but the reserve settlement behind it still operates on banking hours and depends on pre-funded balances at the central bank.

Stablecoins have a structural advantage here. Because they are bearer instruments backed by a reserve pool (not bank deposits), they do not require reserve settlement at every hop. A USDC transfer from wallet A to wallet B on a public blockchain settles when the blockchain confirms the transaction. No central bank window required.

This is what the Banking Exchange guide identified as the "key differentiator" that explains "why certain segments of the market will opt for stablecoins" even as banks build tokenized deposit infrastructure (Banking Exchange, Jan 2026).

The interbank tokenized deposit problem is not unsolvable. Several projects are working on it. But none are in production at scale in the US as of mid-2026.

Who is building what

The institutional activity is real, even if the interbank piece is still missing.

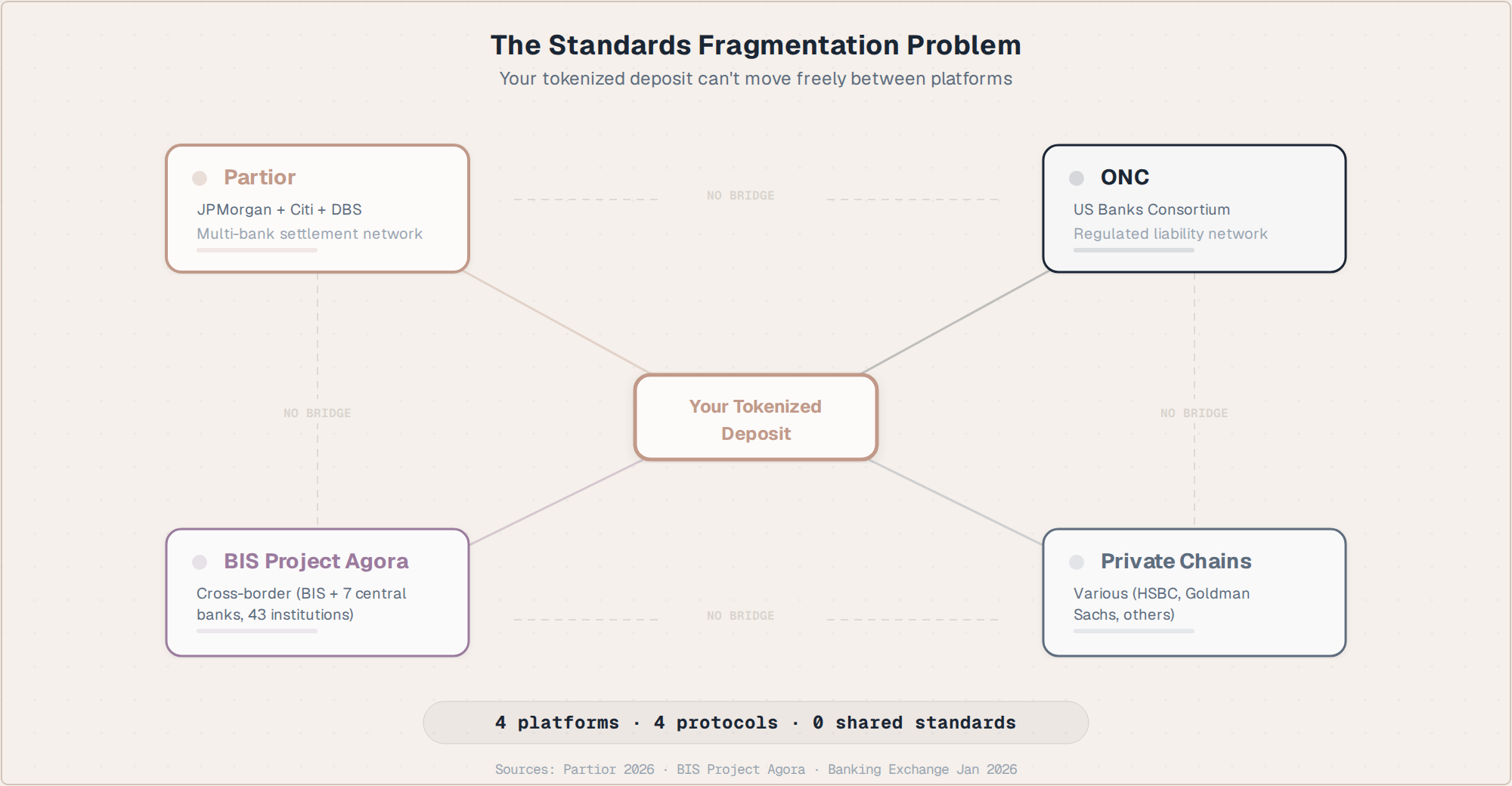

JPMorgan is the furthest along. Its Kinexys platform (formerly JPM Coin) crossed $1.5 trillion in cumulative tokenized deposit value by spring 2025 (Forbes, May 2025). JPMD launched on Base, a public Ethereum Layer 2, in November 2025, making JPM the first major bank to issue a deposit token on a public blockchain (JPMorgan, Nov 2025). JPM is also live on Partior, a Singapore-based interbank payment network it co-founded with DBS Bank, Temasek, and Standard Chartered (Ledger Insights, Dec 2023).

Citi has integrated its blockchain-based Citi Token Services with 24/7 USD Clearing, addressing the interbank payment limitation for its own clients (Citi, Nov 2025). Citi's Regulated Liability Network allows corporate treasurers to sweep cash across borders without the traditional chain of correspondent bank hops.

Goldman Sachs and BNY Mellon launched tokenized money market funds on GS DAP, Goldman's private blockchain platform, in July 2025 (Goldman Sachs, Jul 2025).

HSBC has extended tokenized deposit services to corporate clients, including in the US (American Banker, Apr 2026). BMO and the UK's Monument Bank have announced tokenized deposit offerings as well.

The regulatory chessboard

Regulation is not determining the winner. It is shaping the rules of play.

United States: The GENIUS Act (July 2025) created a federal framework for payment stablecoins, ending years of ambiguity. The OCC issued Interpretive Letters 1186 and 1188 in late 2025, confirming that national banks can hold crypto assets for operational purposes and engage in riskless principal crypto transactions. Together with SAB 121's rescission, US banks now have a clear path to issue both tokenized deposits and stablecoins without pre-clearance hurdles.

European Union: MiCA takes a different approach. Large-scale stablecoin issuance requires e-money institution licensing, and daily turnover caps apply unless the issuer meets additional requirements. The framework exists, but it is more restrictive than the US approach.

Singapore: The DTSP regulations took effect June 30, 2025. MAS "has set the bar high for licensing and will generally not issue a licence" for extraterritorial DTSPs, citing higher money laundering risks (Singapore Statutes, May 2025).

Japan: Japan's ruling LDP pushes stablecoins and tokenized deposits as instruments of "on-chain financial sovereignty" (Decrypt, May 2026). MUFG, SMBC, and Mizuho are jointly piloting stablecoin issuance under an FSA sandbox (FinanceFeeds, May 2026).

BIS Project Agora: Seven central banks and 41 financial institutions are testing a unified ledger for tokenized cross-border payments. The project moved from design to real-world testing in January 2026 (BIS; Ledger Insights, Jan 2026).

The numbers people quote

Stablecoin supply exceeded $310 billion as of January 2026 (Banking Exchange, Jan 2026). Transaction volume in 2025 was estimated at $62 trillion, according to BCG data cited in Deutsche Bank's May 2026 whitepaper (Deutsche Bank / FintechNews, May 2026).

That $62 trillion figure needs context. Deutsche Bank's own whitepaper estimated that only about 7% of stablecoin activity in 2025 was real-economy payments. The rest was trading, DeFi, and speculative flows. The real-economy share grew roughly 55% year over year and was strongest in B2B, but the headline number overstates commercial adoption.

McKinsey puts annual cross-border payment friction at $120 billion (Forbes, May 2025). Citi predicts the total market for digital money instruments could reach $4 trillion by 2030 (Banking Exchange, Jan 2026). EY-Parthenon found that 54% of institutional non-users plan to adopt stablecoins within 6 to 12 months.

These are big numbers. They tell you the market is real and growing. They do not tell you which form of tokenized money wins, because winning is the wrong frame.

Coexistence, not replacement

The NY Fed's February 2026 staff report by Xuesong Huang and Todd Keister modeled the economics precisely. When regulatory costs are high and banks' risk-shifting incentive is limited, tokenized deposits alone maximize welfare by expanding credit. When regulation is lighter and risk-shifting is strong, stablecoins alone perform better despite crowding out bank credit. "In between these cases, allowing stablecoins and tokenized deposits to compete is optimal" (NY Fed Staff Report 1179, Feb 2026).

Corporate treasurers are already behaving this way in practice. Forbes described how treasurers "are already splitting their stakes: deposit tokens for intra-bank liquidity; stablecoins for Saturday-night invoices in Buenos Aires" (Forbes, May 2025).

Kapron's analogy is better than most: "This isn't VHS versus Betamax. It is more like Wi-Fi and Ethernet, competing, interoperable, increasingly invisible."

What is actually unresolved

Several pieces of the architecture have working pilots and institutional backing. Others are genuinely open questions.

Interbank tokenized deposit settlement. This is the biggest gap. Partior in Singapore is the closest thing to a multi-bank tokenized deposit network, and it is still early-stage. Until tokenized deposits can settle between different banks on-chain without falling back to reserve rails at every hop, their advantage over traditional payments is speed within a single institution, not systemic change.

Who controls the standard. TCMAG published Core Principles for Digital Money in April 2026 (TCMAG). BIS is pushing the Agora unified ledger. JPMorgan plans to open Kinexys to third-party banks. The standard that wins will determine who controls the programmability layer. That is the actual competition, not banks versus crypto.

Central bank participation. If wholesale CBDC becomes the settlement layer for interbank tokenized deposits, the interbank gap has a path to resolution. But wholesale CBDC is itself still in testing. The ECB's digital euro timeline (pilot H2 2027, possible launch 2029) shows how long these timelines run.

Stablecoin run dynamics. The USDC de-peg during the SVB collapse in March 2023 was a warning. Tether booked more than $5 billion in profit during the first half of 2024 from the spread between Treasury yields and the zero interest paid to holders. That profit captures value that, in a tokenized deposit, would flow to the depositor. It is also a political target.

What to watch

The market is not waiting for interbank tokenized deposits to be solved before it moves. Stablecoins are already moving tens of trillions in annual volume, with real-economy use growing faster than speculative use. Banks are building tokenized deposit rails for the flows they already control and that need regulatory certainty.

The question is not which wins. The question is whether the interbank tokenized deposit gap closes fast enough for bank-issued tokens to compete on reach, or whether stablecoins capture enough of the corporate treasury market that banks end up issuing stablecoins themselves.

Japan's three largest banks are already doing exactly that. The US approach lets banks choose their own adventure. Singapore's DTSP framework makes the licensing bar high enough that only serious operators will enter.

Five to seven years is a reasonable timeline for this to shake out. Not this year. Not next. The infrastructure is being built now. The standards battle is the one worth watching.

Sources cited in this article were verified as of May 2026. Full source inventory: 22 verified sources across industry publications, official institutional releases, central bank research, regulatory documents, and specialist media.