Digital Identity in Payments: The Invisible Layer Before Money Moves

The 200-Millisecond Question

What happens when you tap your contactless card at a payment terminal?

The transaction takes about 200 milliseconds. Most of that time is not spent moving money. It is spent answering a question the terminal asks every time: who are you?

You do not see this question. The terminal does not print it on the screen. But behind that tap, four separate identity checks are running. The card's chip proves it is genuine (not a clone). The token stored on the chip proves it was issued to you (not someone else). The terminal verifies the merchant's identity with the acquirer. And the network checks that the merchant is allowed to accept this type of card.

All of this happens before the authorization message even reaches your bank.

Identity is the invisible layer in every payment. Not a compliance checkbox. Not a one-time onboarding step. A continuous verification stack that runs from the moment you open a bank account to the moment you tap your card at a checkout counter.

And here is the part most practitioners miss: the identity systems running these checks were never designed to talk to each other.

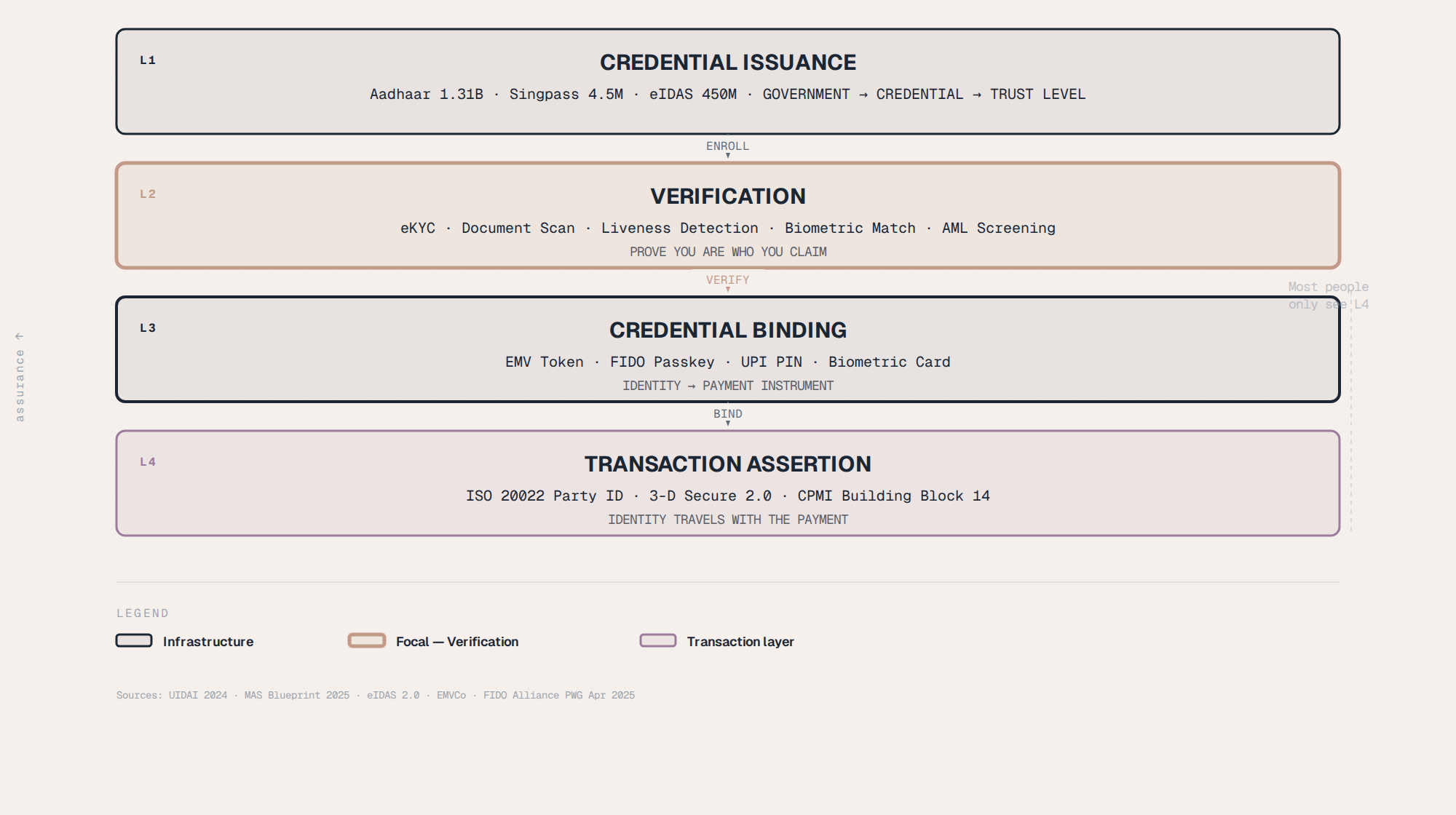

The Four Layers of Identity Assurance

Every payment transaction relies on four identity layers stacked on top of each other. They look sequential on paper. In practice, they run concurrently, and each one uses a different trust model.

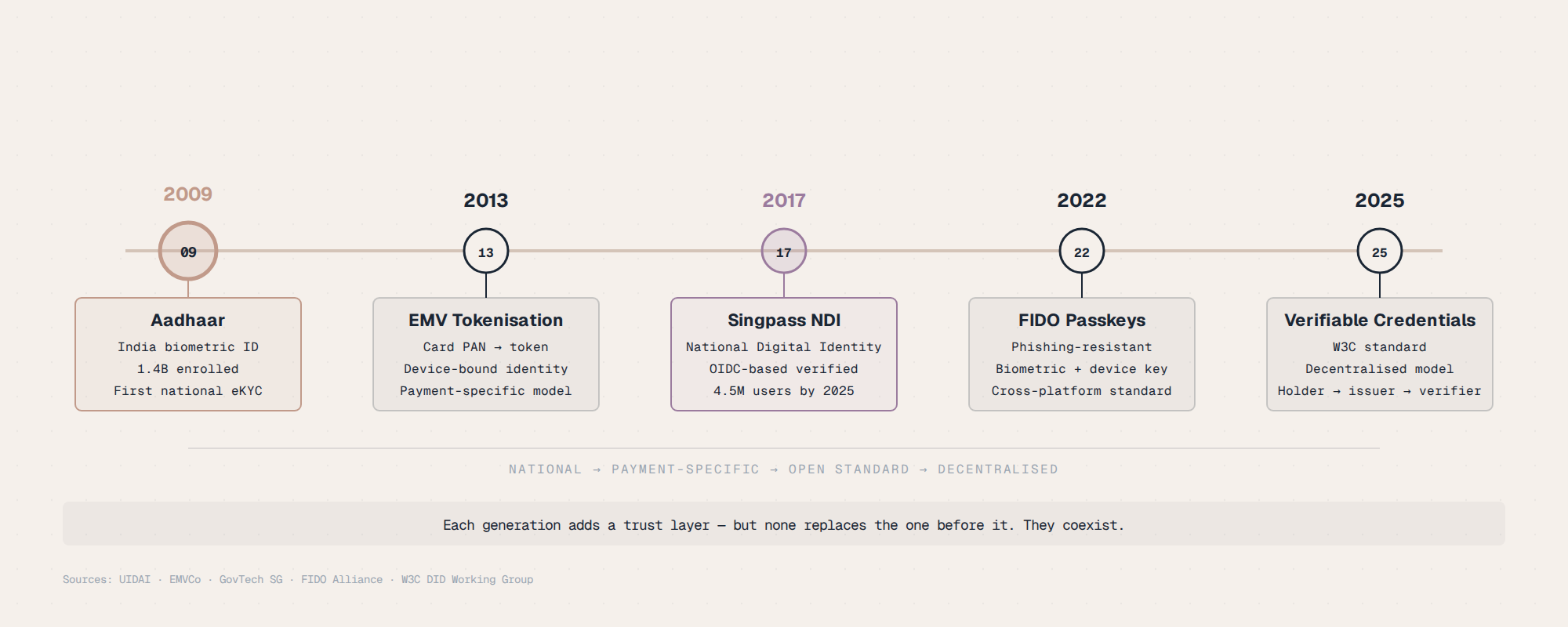

Layer 1: Credential Issuance.A government or trusted institution creates a digital credential that says "this person exists and here is who they are." India's Aadhaar system has enrolled 1.31 billion people using biometric data (fingerprints and iris scans). Singapore's Singpass provides 4.5 million citizens with a National Digital Identity linked to their NRIC. The EU is building the European Digital Identity Wallet for 450 million citizens, due by December 2026. Each credential has a different assurance level. The US NIST framework calls this IAL, or Identity Assurance Level, ranging from IAL1 (self-asserted, you just type your name) to IAL3 (verified in person with physical documents).

Layer 2: Verification.When you open a bank account or register for a payment service, someone has to check that the credential is real and belongs to you. This is eKYC, or electronic Know Your Customer. Aadhaar's eKYC lets a bank verify your identity remotely using a fingerprint or iris scan matched against the UIDAI (Unique Identification Authority of India) database. Singpass uses face verification: you scan your face, the system matches it against your NRIC photo. The EU wallet will use Qualified Electronic Signatures, a cryptographic proof that the wallet holder is who they claim to be. Each verification method has a different trust anchor. Aadhaar trusts a central government database. FIDO trusts a hardware security key built into your phone. These are fundamentally different assumptions about where trust lives.

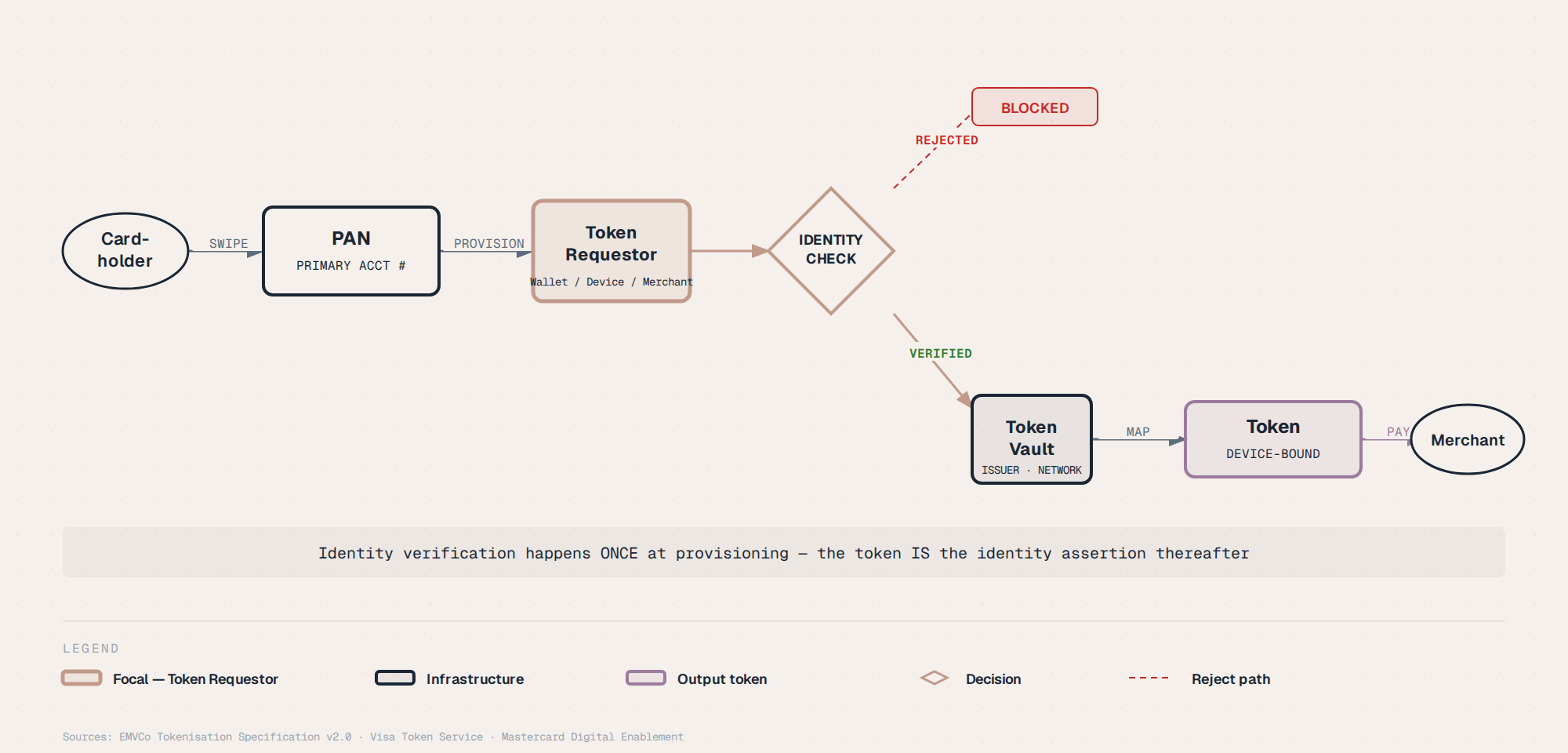

Layer 3: Binding.Once your identity is verified, it needs to be linked to a payment instrument. This is the binding layer, and it is where most of the architectural diversity lives. EMV tokenization (the system behind Apple Pay and Google Pay) replaces your actual card number with a token. The token requestor (Apple, Google) verifies your identity before the issuer provisions that token. FIDO passkeys bind your identity to a specific device using a hardware-backed cryptographic key. UPI binds your Aadhaar-verified mobile number to your bank account. Biometric payment cards store a fingerprint template directly on the EMV chip. Each binding creates a different type of trust assertion. A FIDO passkey says "this specific device vouches for this person." An EMV token says "this issuer has verified this person and linked them to this token." An Aadhaar-linked UPI address says "this mobile number has been biometrically verified against a national database."

Layer 4: Transaction.When the payment actually happens, identity data travels with the message. ISO 20022, the messaging standard replacing SWIFT MT and ISO 8583, defines structured party identification fields. These can carry a Legal Entity Identifier (LEI), a Business Identifier Code (BIC), a national ID number, or a structured name and address. The CPMI (Committee on Payments and Market Infrastructures, part of the Bank for International Settlements) has identified identity data harmonization as Building Block 14 in the G20 cross-border payments roadmap. 3-D Secure 2.0, the protocol behind "verify your identity" popups during online checkout, is moving toward FIDO passkey challenges instead of one-time passwords. But the identity data in the message and the identity check during authentication are two separate things. The message says who you claim to be. The authentication proves it.

The Trust Model Mismatch

Here is where the architecture breaks down.

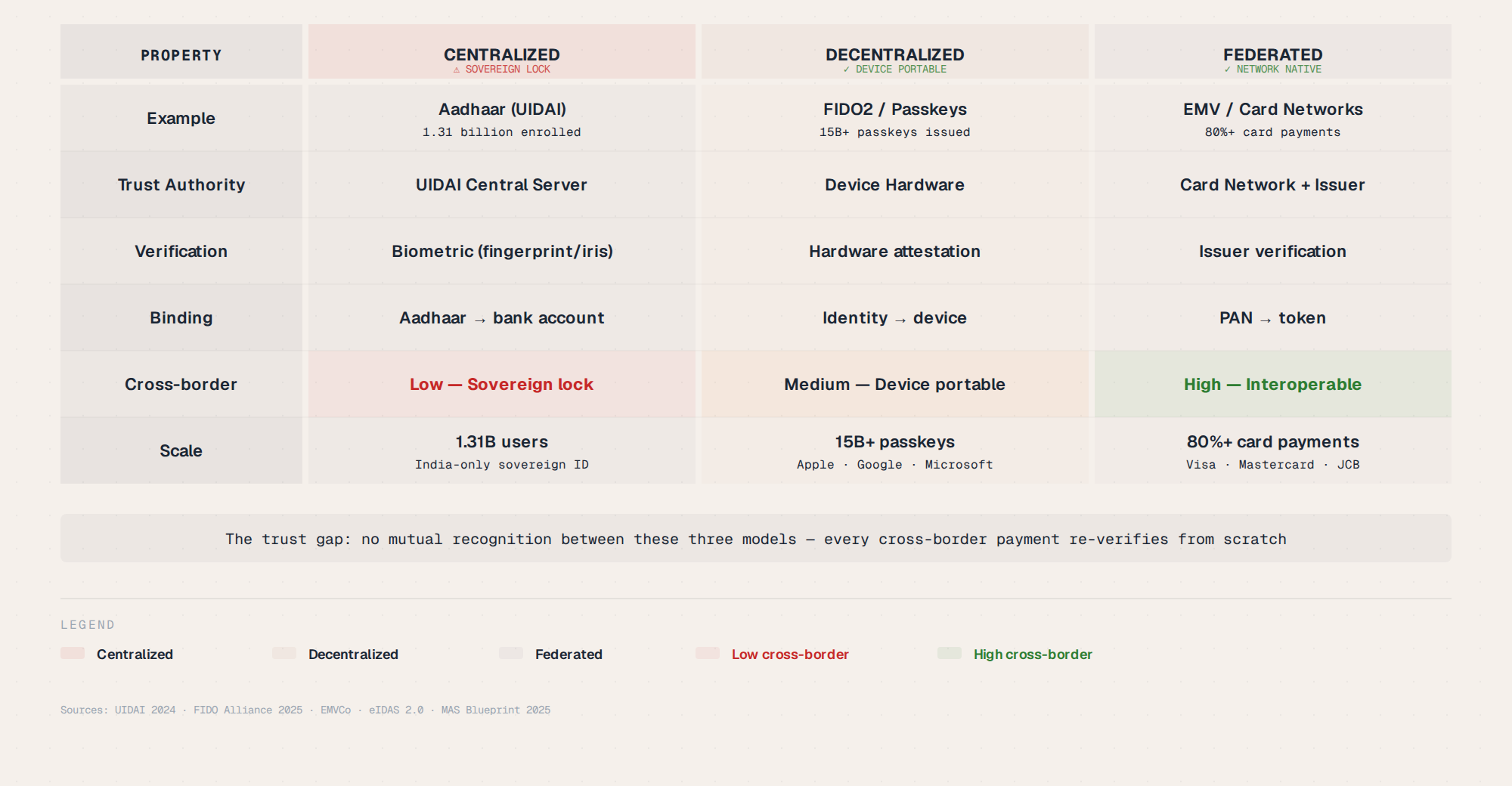

Aadhaar uses centralized biometric authentication. Your fingerprint is matched against the UIDAI database. Trust flows from a central authority.

FIDO uses decentralized device attestation. Your phone's security chip generates a cryptographic proof. Trust flows from the hardware.

EMV uses issuer-verified token binding. Your bank confirms your identity before provisioning a token. Trust flows from the issuing institution.

These three trust models are architecturally incompatible. They make different assumptions about who holds the truth, how verification happens, and what constitutes proof.

Domestically, this does not matter. Aadhaar works within India.

Singpass works within Singapore. FIDO works with any service that accepts passkeys.

Each system is internally consistent.

The failure mode shows up at the border.

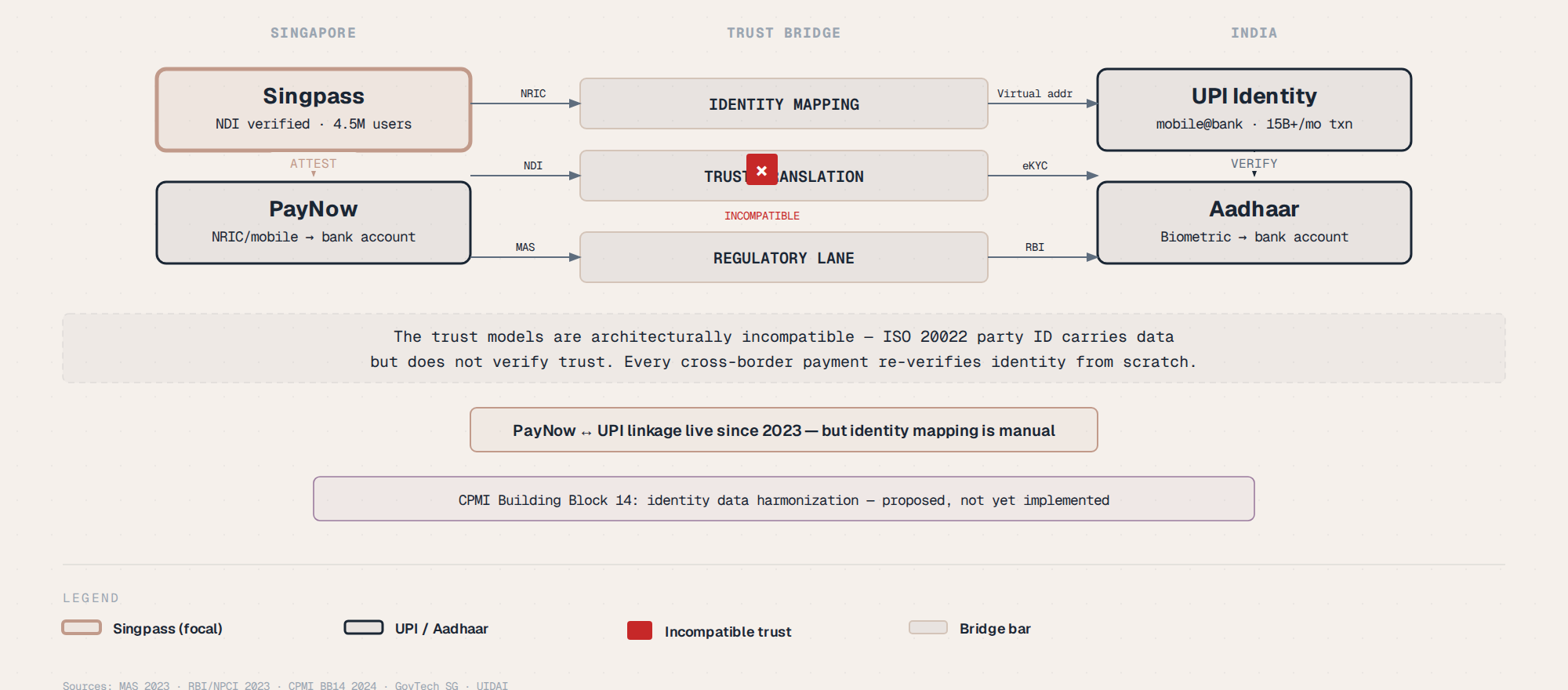

When PayNow Meets UPI

Singapore and India linked their instant payment systems in 2023. PayNow users can send money directly to UPI users, and vice versa. From the user's perspective, it feels like sending money to someone in the same country.

Under the hood, two sovereign identity systems have to agree on who both people are.

The sender's identity is verified by Singpass. Singpass links their NRIC (National Registration Identity Card) to their mobile number, which is linked to their bank account via PayNow.

The receiver's identity is verified by Aadhaar. Aadhaar links their biometric data to their mobile number, which is linked to their bank account via UPI.

When the payment crosses the border, the identity data has to be translated. The Singpass NRIC assertion ("this person is verified by Singapore's National Digital Identity") needs to be understood by a system that only recognizes UIDAI biometric assertions ("this person is verified by India's biometric database").

This is not a messaging problem. ISO 20022 can carry both identity types in its party identification fields.

This is a trust problem. The receiving system has no native way to verify the sender's Singpass assertion, because it was not built to trust Singapore's identity infrastructure.

It was built to trust India's.

The current workaround is bilateral agreements between the participating banks and payment system operators. Each side agrees to trust the other's identity verification.

But this does not scale. Every new cross-border linkage requires a new trust agreement, and each one is bespoke.

Singapore: Identity to Payment in One Stack

Singapore is the closest thing to a fully integrated identity-to-payment system in production.

Singpass, operated by GovTech Singapore, serves as the credential issuance and verification layer. When you open a bank account in Singapore, the bank can verify your identity through Singpass instead of scanning physical documents. Over 4.5 million users are enrolled.

PayNow, operated by the Association of Banks in Singapore, serves as the binding layer. It links your Singpass-verified NRIC or mobile number to your bank account. When someone sends money to your mobile number, PayNow resolves it to your bank account using the identity already verified by Singpass.

MAS (the Monetary Authority of Singapore) has proposed a "name service" as part of its blueprint for digital money. This name service is essentially an identity resolution layer.

It maps human-readable names to payment addresses, similar to how DNS maps domain names to IP addresses. The blueprint positions identity not as a prerequisite for payments but as a building block of the payment infrastructure itself.

This is architecturally coherent. Identity, binding, and payment addressing all live within the same trust framework.

But it only works within Singapore's borders. The moment money needs to cross to a different identity system, the coherence breaks.

India Stack: 1.31 Billion Identities, 15 Billion Monthly Transactions

India's approach is the largest identity-for-payments deployment ever built.

Aadhaar, launched in 2010, has enrolled over 1.31 billion people. That is 95 percent of India's population. Each enrollment captures biometric data (ten fingerprints, two iris scans, a face photo) and demographic information.

The India Stack extends Aadhaar into a set of APIs for financial services. eKYC allows banks to verify customer identity remotely.

eSign provides Aadhaar-based digital signatures. DigiLocker stores verified digital documents (degrees, vehicle registrations, tax returns).

UPI (Unified Payments Interface) uses Aadhaar-linked mobile numbers as payment addresses. When you register for UPI, your mobile number is verified against your Aadhaar-linked bank account.

Your identity is already bound to your payment instrument. You do not need a separate identity verification step for each transaction.

The result: UPI processes over 15 billion transactions per month. The identity verification happens once, at enrollment, not at every transaction.

This is a design choice. India chose to front-load the identity check (strong verification at enrollment, lightweight authentication at transaction time) rather than re-verify identity for every payment.

This works because India controls the entire stack. One identity system.

One payment system. One set of APIs.

The trust model is internally consistent.

What Is Coming: 2026-2028

Three developments will reshape the identity layer in payments over the next two years.

The EU Digital Identity Wallet.By December 2026, all 27 EU member states must offer a digital identity wallet under eIDAS 2.0 (Regulation EU 2024/1183). The wallet stores identity credentials, payment instruments, and qualified electronic signatures. It uses W3C Verifiable Credentials (a standard for cryptographically verifiable digital credentials) with selective disclosure, meaning you can prove you are over 18 without revealing your exact birth date. For payments, the wallet can satisfy PSD2 and PSD3 Strong Customer Authentication requirements without separate OTP or biometric checks. The identity is already in the wallet. The wallet is already verified.

FIDO passkeys for card payments.The FIDO Alliance launched a Payments Working Group in April 2025. Visa and Mastercard are participating. The goal is to standardize passkey-based authentication for card-not-present transactions, account-to-account payments, and peer-to-peer transfers. This would replace the 3-D Secure challenge flow (OTP, biometric prompt from your bank) with a passkey verification. The trust model shifts from "your bank sends you a code" to "your device cryptographically proves your identity."

Post-quantum identity migration.NIST finalized its post-quantum cryptography standards in 2024: ML-KEM for key encapsulation and ML-DSA for digital signatures. Every digital signature currently authenticating payment identities uses math that a sufficiently powerful quantum computer could break. The migration timeline is 5 to 10 years, but the planning needs to start now. Yubico's latest security keys already support hybrid post-quantum authentication. The question is not whether the identity infrastructure needs upgrading. The question is whether the upgrade can happen before the threat materializes.

The Unsolved Problem: Trust Model Interoperability

Every domestic identity system works. India's Aadhaar processes billions of identity assertions per month.

Singapore's Singpass underpins one of the highest digital payment adoption rates in the world. The EU's wallet will create a unified identity layer across 27 countries.

The unsolved problem is between them.

When identity systems cross borders, they carry incompatible trust assumptions. Aadhaar trusts a centralized biometric database.

FIDO trusts a hardware security key. EMV trusts an issuer's verification.

ISO 20022 party identification fields can carry identity data across borders, but they cannot verify it. They are the address on the envelope, not the signature inside.

W3C Verifiable Credentials offer a structural path forward. A verifiable credential is a cryptographically signed claim that a verifier can check without contacting the issuer. If India issued Aadhaar verification as a W3C Verifiable Credential, and Singapore's PayNow system could verify that credential's cryptographic signature, the two systems could interoperate without bilateral trust agreements.

But this requires standards adoption, legal recognition, and a governance framework for cross-border credential verification. None of that exists today at scale.

Identity is not a compliance checkbox. It is not a one-time onboarding step. It is the payment infrastructure nobody builds for until cross-border breaks.