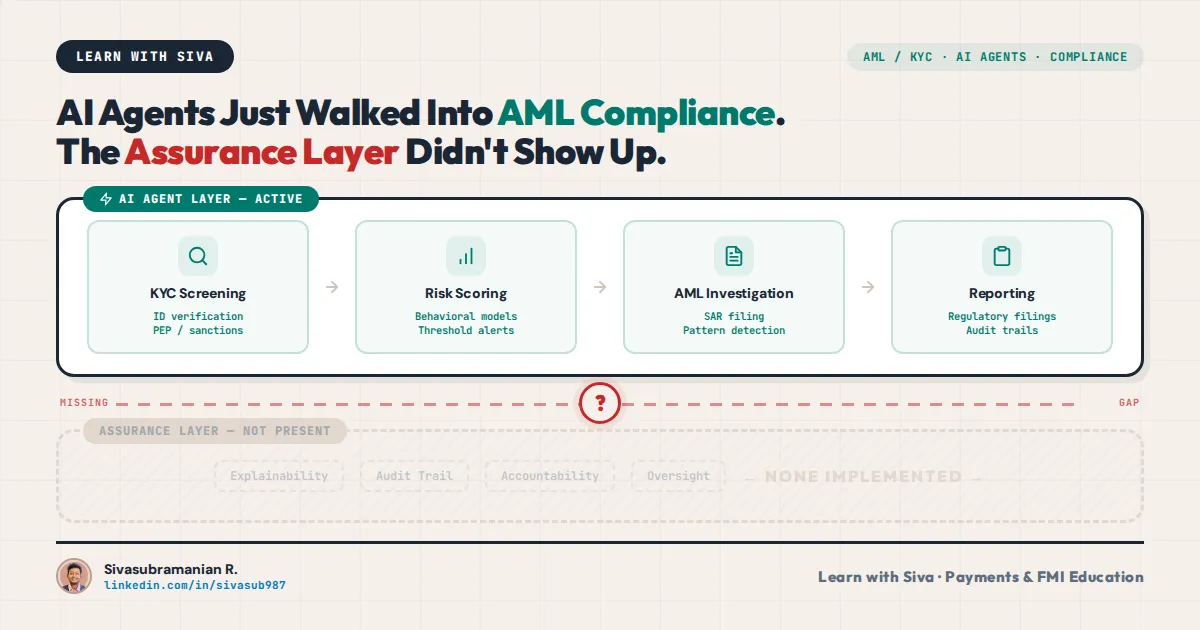

AI Agents Just Walked Into AML Compliance. The Assurance Layer Didn't Show Up.

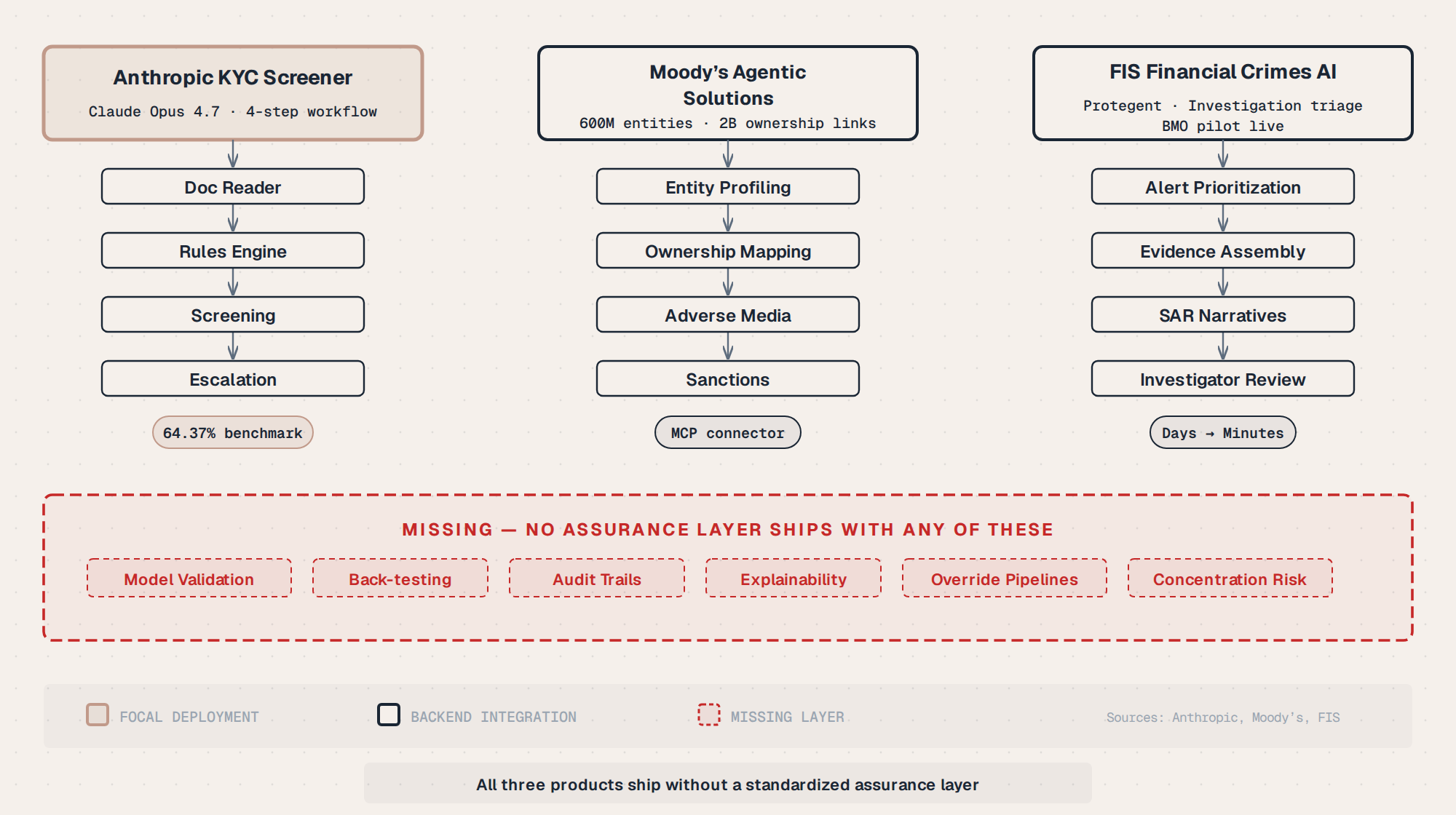

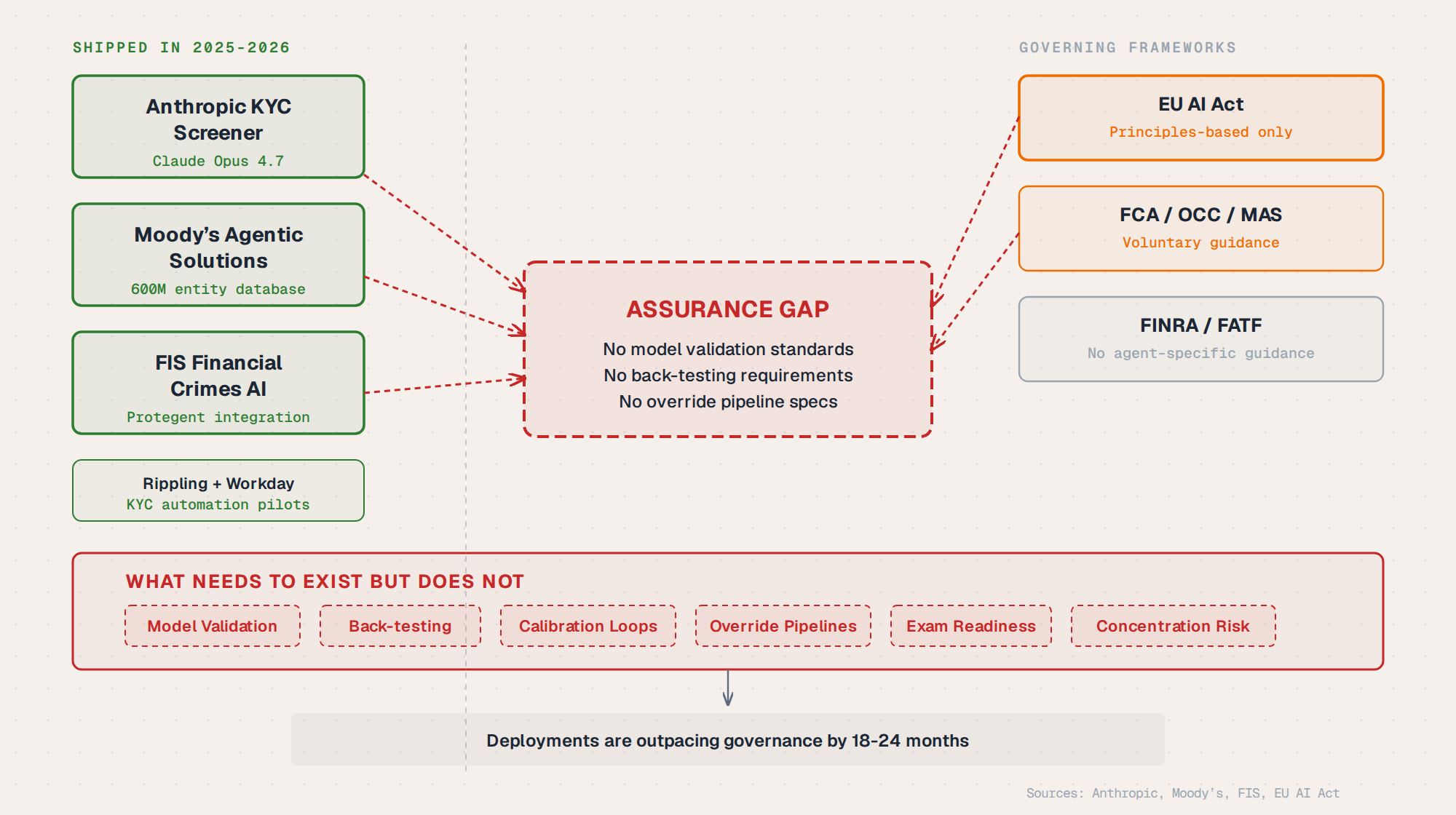

Four announcements landed in a single month. Anthropic shipped ten ready-to-run agent templates for banks, including a KYC screener. Moody's connected 600 million company records directly into Claude. FIS embedded AI into AML investigations at BMO, compressing triage from days to minutes. Blackstone, Goldman Sachs, and H&F launched a $1.5 billion enterprise AI services company (Source).

That's a lot of velocity for an industry where a single missed SAR filing can trigger a civil penalty of $25,000 per day (Source). The agents are real. The capabilities are impressive. But the gap between what these agents can do and what regulators will accept is the actual problem, and nobody's building the bridge.

What Actually Landed

Let's be specific about what shipped, because the gap only makes sense if you see the capability boundary clearly.

Anthropic's KYC Screener runs a four-step workflow: document reading via vision/OCR, a rules engine that applies firm-specific KYC/AML policy, a screening step that checks named parties against sanctions and PEP lists, and an escalation step that bundles anything needing human attention into a compliance packet (Source). The output is structured JSON with risk rating, disposition, and rule outcomes. It runs in three modes: alongside the analyst in a browser, in a terminal, or autonomously on Anthropic infrastructure with credential vault and full audit log (Source).

What it doesn't ship with is the hard part. No document forensics. No ID tampering detection, font analysis, hologram verification, or fraudulent rendering detection. No liveness or deepfake detection. No device intelligence or behavioral biometrics. No KYB or UBO checks. No pre-built CIP rule library with back-testing frameworks. No case management UI. No ongoing monitoring, re-screening, or risk rating updates (Source). As Chen Zamir at Sardine put it: "Anthropic is shipping the reasoning layer. The bank, or the vertical KYC vendor the bank is using, ships the data, signals, forensics, and operational substrate the reasoning runs on top of."

Claude Opus 4.7 scored 64.37% on Vals AI's Finance Agent benchmark. That's described as "industry-leading," which means the best anyone has done is still failing a little more than a third of the time (Source).

Moody's + Claude is a different kind of integration. Moody's Agentic Solutions runs natively in the Claude environment through a purpose-built Model Context Protocol application, surfacing 600 million entities and 2 billion ownership links for entity profiling, ownership structure mapping, adverse media screening, and sanctions checks (Source). Client data stays within Moody's/FIS-controlled infrastructure. Claude operates as the reasoning layer, one step removed from source data. The outputs render as interactive reports directly within Claude, which is genuinely useful.

But "outputs are valid, explainable, and auditable to meet the standard required for high-stakes decision-making in regulated environments" is a press release claim, not a third-party audit. You won't find a regulatory certification or a standardized benchmark result behind that language. It's Moody's saying their own outputs are good enough.

FIS + BMO is the most operationally concrete of the three. FIS powers nearly 12% of the global economy by transaction volume, and their Financial Crimes AI Agent compresses AML investigation triage and evidence assembly from hours or days down to minutes (Source). It evaluates activity against known financial crime typologies, improves SAR narrative quality, and surfaces only the highest-risk cases for investigator review. BMO and Amalgamated Bank are the first development partners, with broader availability planned for the second half of 2026.

This isn't end-to-end SAR filing. It's the triage and evidence-gathering phase, the part where investigators spend most of their time manually assembling evidence across disconnected systems. That's a real bottleneck and a real win. But "days to minutes" measures speed, not accuracy. It doesn't tell you whether the agent correctly identified which cases to surface and which to deprioritize.

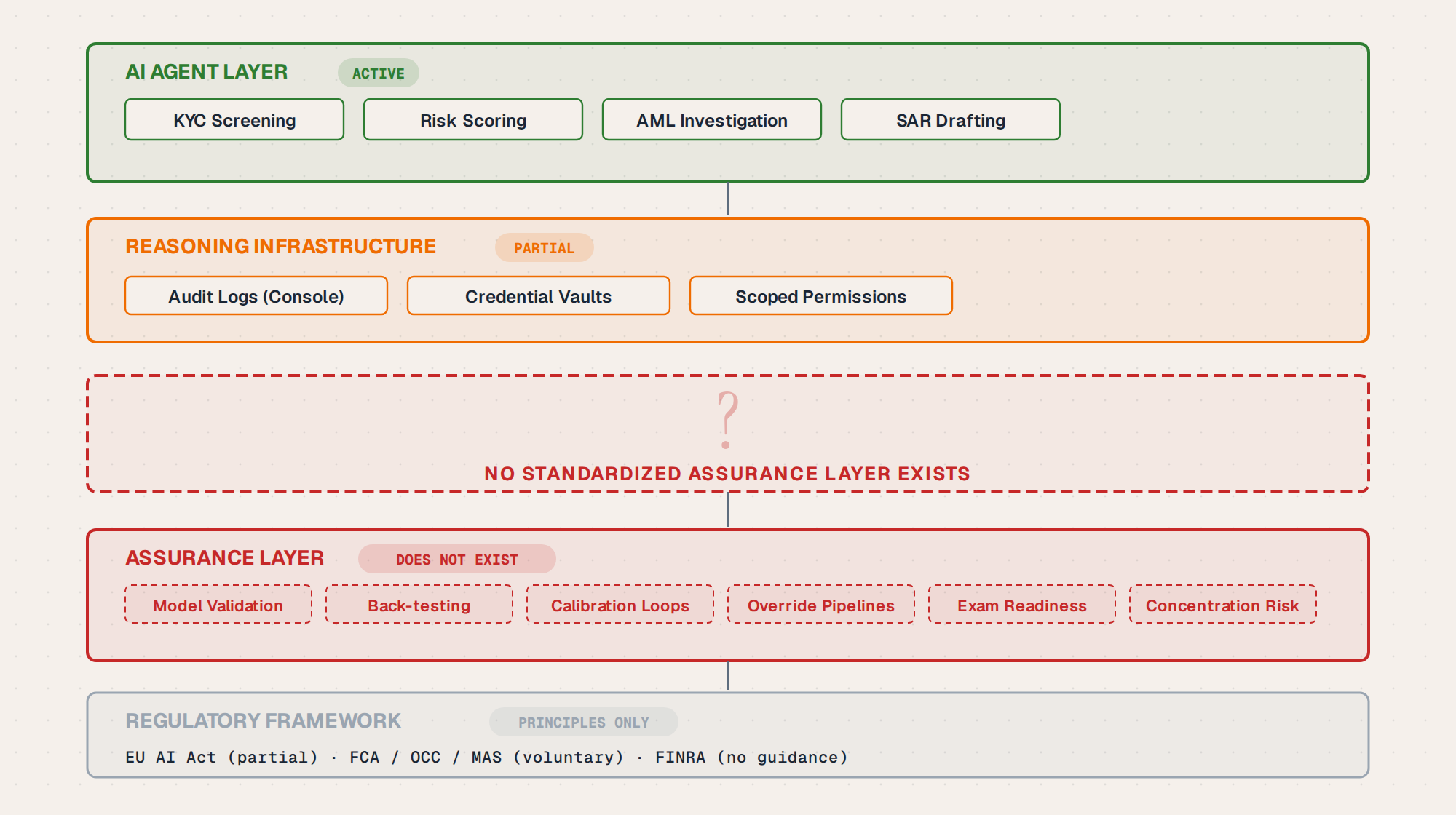

What's Missing: The Assurance Layer

An audit log is not a case manager. A case manager is the substrate where the agent's decisions, the analyst's overrides, the customer's evidence, the timeline of communications, the escalation paths, and the feedback loop into the next model version all live. It's where a regulator points when they ask: show me how you decided to clear this customer (Source).

Anthropic's Managed Agents provide per-tool credential vaults, scoped permissions, and full audit logs in Claude Console. Those are necessary infrastructure. They are not sufficient assurance. Here's what's missing from the ecosystem:

No model validation for compliance use cases. There's no standardized framework for testing whether a compliance agent meets accuracy thresholds for production deployment. The 64.37% benchmark score is the best available, and it comes from Vals AI, not from a regulator or a standards body.

No back-testing frameworks. No standard way to test an agent against historical true positives and true negatives with 30/60/90-day windows. Banks have years of SAR filing history. That data should be the test set. Nobody has agreed on how to build it.

No calibration loops. LLMs tend to flag too many things as suspicious without calibration to specific customer bases. What counts as "normal" at a community bank in Iowa looks different from what counts as "normal" at a private bank in Singapore. There's no standardized approach to training agents on institution-specific baselines.

No analyst override and disagreement pipelines. When an analyst disagrees with an AI decision, that disagreement needs to be captured, logged, and fed back into model improvement. That infrastructure doesn't ship with any of the current agent templates.

No regulatory examination readiness. No standard format exists for presenting AI compliance decisions to regulators. When an examiner asks how a specific customer was cleared, the answer shouldn't require a custom integration project.

The Regulatory Vacuum

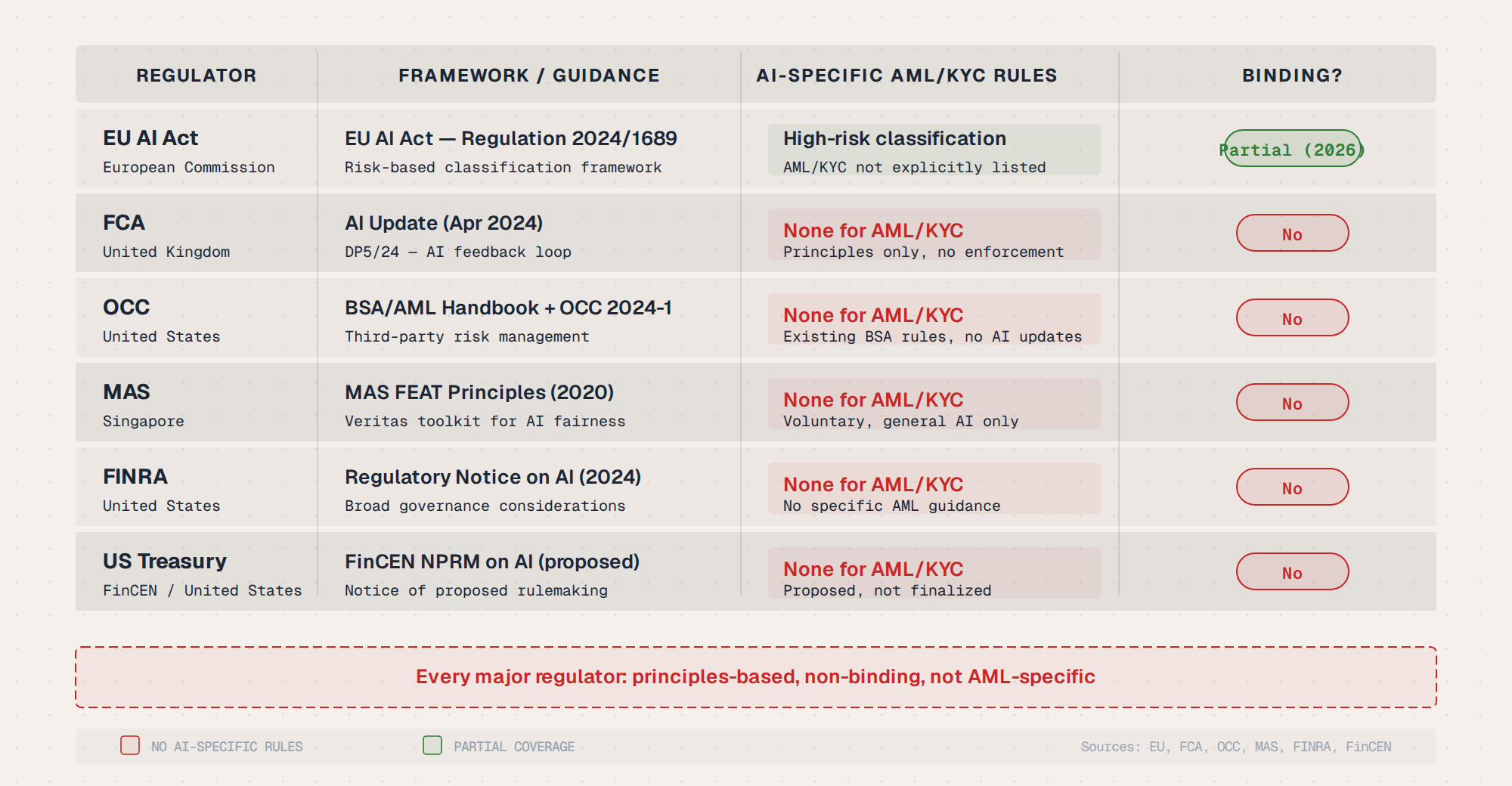

No major regulator has issued binding rules that specifically govern how AI agents must perform in AML/KYC workflows. Everything that exists is principles-based, non-binding, and fragmented.

The EU AI Act is the closest thing to a framework. AI systems in "access to and enjoyment of essential private services" and "management and operation of critical infrastructure" are classified as high-risk. AML/KYC screening could plausibly fall into those categories. High-risk systems must be assessed before market entry and throughout their lifecycle. But the Act isn't AML-specific. It doesn't address SAR filing accuracy, false positive rates, or investigator oversight requirements (Source).

The FCA in the UK acknowledges AI's growing role in financial services but relies on existing regulatory frameworks like the Senior Managers and Certification Regime rather than AI-specific rules. No binding requirements on audit trails for AI-generated compliance decisions (Source).

The OCC in the US addresses AI vendors indirectly through third-party risk management guidance (Bulletin 2021-20), written before agentic AI was a consideration. Banks are expected to manage AI under existing model risk management frameworks (SR 11-7/OCC 2011-12). No AI-specific examination procedures for AML/KYC compliance exist (Source).

MAS published the FEAT Principles (Fairness, Ethics, Accountability, Transparency) for AI in financial services. These are voluntary and principles-based. No specific accuracy thresholds or audit requirements (Source).

FINRA has published reports acknowledging AI adoption in securities. Existing supervision obligations under Rule 3110 would theoretically cover AI-assisted decisions, but no guidance has been issued on what "reasonable supervision" of an AI agent looks like.

The US Treasury chief publicly urged bank executives to approach Anthropic's recent AI releases with caution in late April 2026. The signal is unmistakable: regulators are watching the pace of deployment, and they are not yet certain the controls match the capability (Source).

The summary is blunt. No binding standards on AI accuracy for AML/KYC tasks. No mandatory audit trail requirements for AI-generated compliance decisions. No explainability standards. No liability framework assigning responsibility when AI agents make compliance errors. No certification or validation regime before deployment. Everything is principles-based and non-binding.

The Liability Gap: You're Holding the Bag

Under 31 USC § 5318(g), financial institutions are required to report suspicious transactions. Failure to file a SAR can result in civil penalties of up to $25,000 per day of violation, or criminal penalties. The law doesn't distinguish between "our employee missed it" and "our AI agent missed it." The institution is liable either way.

FinCEN has brought enforcement actions for BSA/AML program failures where technology was involved. The enforcement theory is always institutional: the bank failed to maintain an adequate compliance program. No FinCEN enforcement action has specifically addressed AI agent failures yet, but the legal theory is ready. The bank is the respondent, not the vendor.

Anthropic's terms of service for Claude specifically disclaim liability for outputs. The financial services agents documentation states that "users stay firmly in the loop, reviewing, iterating on, and approving Claude's work." That's not just a design choice. It's a liability boundary. The bank retains all regulatory liability for AI-assisted decisions.

There's no AI-specific safe harbor for compliance decisions. No shared liability framework between the bank, the AI vendor, and the data provider. No standard of care for what constitutes "reasonable" use of an AI agent in AML. If a human reviewer rubber-stamps AI recommendations, is that adequate supervision? Nobody has answered that question, and the answer won't come from a vendor's terms of service.

The cross-jurisdictional problem adds another layer. If a Claude-based AML agent processes data across borders, which jurisdiction's liability framework applies? The Moody's MCP integration adds another wrinkle: if Moody's data is wrong and Claude acts on it, who's liable? These aren't theoretical questions. They're operational questions that banks need answered before deployment.

What a Proper Assurance Framework Would Look Like

Nobody has built this yet. Here's what it would need:

Standardized test sets. Curated sets of true positive and true negative cases for AML/KYC tasks, with ground truth labels. Banks have the historical data. Someone needs to build the shared benchmark.

Accuracy benchmarks with minimum thresholds. Specific, binding requirements for false positive rates, false negative rates, and processing time. "Industry-leading at 64.37%" is a marketing statement. A threshold is a regulatory requirement.

Explainability requirements. Minimum standards for what an AI agent must be able to explain about its decisions. Not "the model can generate natural language explanations." Specific requirements about what information must be included in those explanations.

Audit trail standards. A common format for logging AI compliance decisions that regulators can examine without custom integration work. The audit log in Claude Console is proprietary. Regulators need a standard they can query.

Feedback loop requirements. Mandatory analyst override capture and model retraining pipelines. When an analyst disagrees with the agent, that signal needs to flow back into the model automatically, not disappear into a spreadsheet.

Concentration risk management. Multiple banks running AML agents on the same Claude infrastructure creates a single point of failure across the financial system. That needs governance, and it can't come from the vendor alone.

What This Means Operationally

The agents are shipping. BMO and Amalgamated Bank are already development partners. Moody's has connected 600 million entities. The reasoning layer works. The question isn't whether AI agents will be part of AML/KYC workflows. They already are.

The question is what happens between now and when the assurance layer catches up. Banks deploying these agents are absorbing regulatory risk that their vendors won't share. They're building compliance processes around tools that have no certification, no validation regime, and no standardized audit format. They're doing this with the explicit caution of the US Treasury ringing in their ears.

The banks that treat these agents as reasoning engines that need operational substrate, validation infrastructure, and audit-ready case management will be fine. The banks that treat them as compliance products they can plug in and trust will not be fine. The difference isn't the technology. It's the governance layer around it.

U.S. financial institutions spend $35 to $40 billion annually on AML operations (Source). The UN estimates $2 trillion in illicit funds flow through the global financial system every year (Source). The stakes are real. The agents are real. The assurance layer is not. That's the gap, and it's the one worth paying attention to.